The UAE’s crypto fundraising story starts with a market structure most founders underestimate. In the UAE, 69.1% of Emirati respondents report Binance as their primary exchange, according to a 2024 survey on most-used crypto platforms in the country, and Binance FZE holds a full VARA VASP licence in Dubai (most-used cryptocurrency exchanges in the UAE). That combination matters because fundraising doesn’t happen in a vacuum. It happens where liquidity, user trust, fiat access, and regulatory credibility already exist.

For founders, that changes the question. It’s not just, “What are the best platforms for crypto fundraising in the UAE?” It’s, “Which platform mix gives me the best path to capital without creating a compliance problem I can’t unwind later?”

That distinction is where most market guides fail. They treat fundraising platforms as a simple list. In practice, UAE founders face a more strategic reality. The country is pro-innovation, Dubai is highly attractive for Web3 company formation, and many teams use free zone structures as their operating base. If you’re evaluating setup routes, this Smart Classic guide to DMCC company formation is a useful primer on how founders commonly establish a Dubai presence before tackling licensing and fundraising design.

The opportunity is real. The UAE crypto trading platforms market is valued at USD 1.5 billion based on historical data up to 2024, and the same ecosystem now supports exchanges, regulated crowdfunding, and hybrid fundraising routes that didn’t exist a few years ago (crowdfunding platforms in the UAE). But there’s also a structural gap. Local regulation has matured faster than local token-sale infrastructure.

That’s why the most effective founders don’t think in terms of one platform. They think in stages. They use local credibility, tightly defined investor onboarding, and global distribution only when the legal and technical stack is ready. If you’re building in this market, work with a blockchain infrastructure company that understands token issuance, trading infrastructure, and compliance workflows as one system rather than three separate workstreams.

Introduction The UAE’s Rise as a Global Crypto Fundraising Hub

Analysts increasingly place the UAE among the small group of jurisdictions where a crypto fundraising plan can be built around identifiable regulators, active trading activity, and a workable company formation path rather than pure jurisdiction shopping. For founders, that changes the question. The issue is no longer whether the UAE is crypto-friendly. It is whether a project can translate that favourable environment into a funding structure that is both credible and executable.

Dubai matters because fundraising in Web3 is rarely a standalone capital event. It sits on top of entity setup, investor onboarding, banking access, token design, and distribution strategy. Founders that begin with entity structure usually move first through free zone setup before deciding how far they can push into token issuance and public sale mechanics. For teams comparing those early formation routes, Smart Classic’s DMCC company guide is a useful reference point.

The market offers clear advantages:

- More visible regulatory decision points: founders can assess licensing, investor access, and promotional risk earlier than in jurisdictions where token activity remains loosely defined.

- Multiple capital paths: equity, private token rounds, crowdfunding, and exchange-led distribution can be considered in parallel.

- Cross-border relevance: a Dubai-based vehicle can be positioned for Gulf investors while still speaking credibly to capital in Europe, Asia, and other major crypto markets.

That combination gives the UAE an unusual role. It is not just a destination for local fundraising. It often serves as an operating base for projects that need Middle East credibility without giving up global reach.

The structural gap appears one level below the headline narrative. The UAE has moved faster in regulation and corporate infrastructure than in locally regulated token launchpad development. A founder can often set up the right entity, build local substance, and organise compliant investor intake. The harder step is finding a domestic public token sale venue with the same degree of regulatory clarity and market acceptance.

That gap changes platform selection. In practice, many UAE-based teams do not choose a single fundraising platform. They combine local compliance and corporate credibility with offshore or global token distribution channels once legal, technical, and disclosure work is mature enough to support that move.

For a founder entering the UAE, this is the strategic takeaway: the country is strong at preparing a project for fundraising, but less mature as a self-contained venue for every stage of token issuance. The best route is often hybrid by design, not local-only by default.

Understanding Crypto Fundraising Models ICO vs IDO vs IEO vs STO

Before choosing a platform, define the fundraising model correctly. In the UAE, the model determines not only investor access but also how exposed you are to regulatory ambiguity.

ICO

An Initial Coin Offering (ICO) is a direct token sale run by the project itself, usually through its own website or sale portal. The project controls distribution, pricing, and investor onboarding, but it also carries more responsibility for compliance, disclosure, and trust.

ICOs give founders maximum control. You control the sale mechanics, vesting logic, jurisdiction filters, and investor journey. That sounds attractive until you realise you also inherit every credibility problem the market associates with self-hosted token sales.

For UAE-based teams, an ICO can make sense when the product already has an experienced investor base and strong legal structuring. It’s weaker when trust still depends on a third-party venue.

IDO

An Initial DEX Offering (IDO) is a token sale conducted through a decentralised launchpad or exchange environment. It typically offers faster market access and community reach, but founders must manage higher regulatory uncertainty and fragmented investor onboarding.

IDOs are popular because they compress distribution, community activation, and early trading into one event. They also suit teams building on ecosystems where launchpads are integrally embedded in the user journey.

In the UAE context, the issue isn’t whether IDOs work. It’s whether a UAE-based founder can use one without creating legal tension between local operations and offshore distribution. That’s why teams often need strong token sale architecture, careful jurisdiction screening, and stringent investor controls. Founders exploring token routing and multi-channel distribution usually need to think beyond launch marketing and into blockchain and crypto project distribution.

IEO

An Initial Exchange Offering (IEO) is a token sale conducted through a centralised exchange. The exchange handles part of the investor funnel, listing visibility, and trust layer, while the project benefits from the exchange’s user base and market infrastructure.

For many UAE founders, IEOs are the most intuitive route because they align with how the local market already behaves. Exchange-centred fundraising benefits from existing liquidity expectations, familiar user journeys, and stronger signalling around market readiness.

The trade-off is obvious. You give up more control, accept exchange gatekeeping, and rely on listing criteria you don’t fully control.

STO

A Security Token Offering (STO) is a tokenised fundraising model where the asset is structured with characteristics closer to regulated securities. It prioritises legal clarity and investor rights over pure crypto-native speed and distribution.

STOs tend to appeal to tokenised funds, real-world asset plays, and projects with institutional ambitions. In the UAE, that can be strategically attractive because a security-like framing may align better with serious capital formation than a loosely defined utility-token narrative.

The downside is complexity. STOs usually involve heavier legal design, tighter investor qualification, and slower execution.

Comparison of Crypto Fundraising Models

| Model | Platform Type | Primary Advantage | Key Challenge | Best For |

|---|---|---|---|---|

| ICO | Project-owned sale portal | Maximum control | Trust and compliance burden sits with founder | Established communities |

| IDO | Decentralised launchpad | Fast community access | Regulatory ambiguity | DeFi and community-led tokens |

| IEO | Centralised exchange | Distribution plus credibility | Less founder control | Tokens needing liquidity and exchange visibility |

| STO | Regulated security-style structure | Stronger legal framing | Heavier setup complexity | Asset-backed and institutional products |

A founder shouldn’t choose the trendiest model. Choose the one your legal structure, investor base, and token utility can actually support.

What this means in the UAE

A UAE founder usually isn’t choosing between four equal options. They’re balancing two questions:

- How much regulatory certainty do I need?

- How much distribution can I create without a major local launchpad ecosystem?

That’s why UAE strategy often starts with a compliant base and ends with a selectively global token sale route.

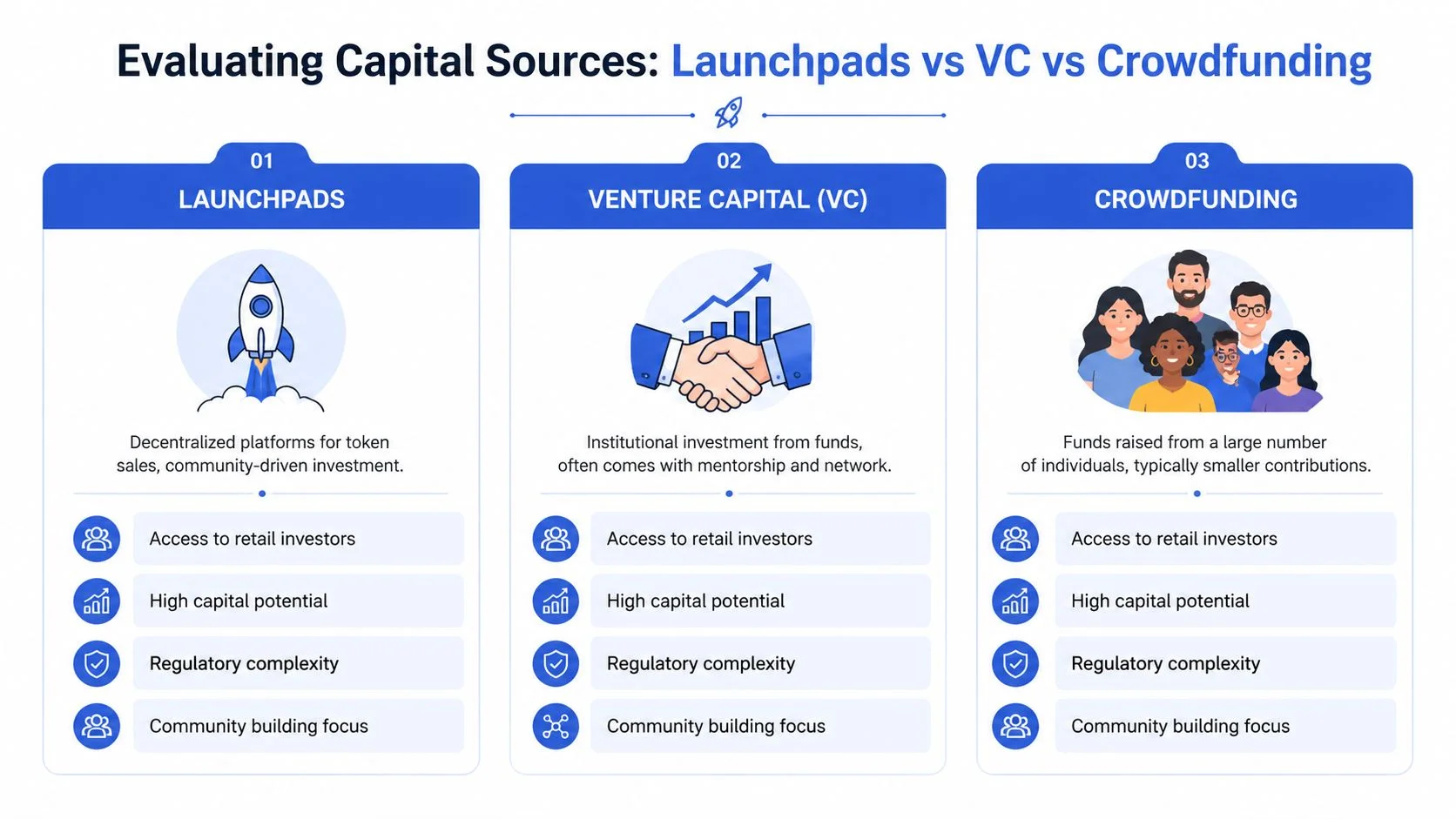

Evaluating Capital Sources Launchpads vs VC vs Crowdfunding

Fundraising model and capital source aren’t the same thing. You can run an IDO and still rely on venture investors beforehand. You can raise through a regulated crowdfunding platform before any token exists. The strongest UAE fundraising plans often combine these routes rather than treating them as substitutes.

Launchpads give distribution, not just capital

A launchpad is useful when your token sale depends on community participation, market visibility, and immediate ecosystem alignment. It’s not just a place to raise funds. It’s a distribution engine.

That matters for protocol tokens, exchange-linked utilities, gaming ecosystems, and community-owned infrastructure. But launchpads are weak if your project still lacks legal clarity, a clear token thesis, or investor onboarding discipline.

Venture capital buys time and signalling

VC is often the right answer before public fundraising, especially for infrastructure-heavy products. If you’re building compliance tooling, exchange infrastructure, trading systems, or institutional workflows, private capital can buy you development time without forcing premature token issuance.

VC is also useful when your cap table needs strategic counterparties rather than broad community access. The trade-off is dilution, governance pressure, and less flexibility in timing your public market move.

Crowdfunding is more relevant than most crypto founders assume

Crowdfunding in the UAE is often dismissed by Web3 teams because it isn’t crypto-native. That’s a mistake. It can serve as a compliant bridge when your product is real, your entity is local, but your token path isn’t yet ready.

The most important local example is DubaiNEXT, the official Dubai Government-backed crowdfunding platform under Dubai SME. It has facilitated AED 50M+ in project funding since launch and reports a 65% success rate for tech ventures, according to UAE government disclosures (Dubai government crowdfunding overview). For a founder, the strategic takeaway isn’t that DubaiNEXT replaces crypto fundraising. It’s that it can de-risk the early round before token distribution becomes appropriate.

Practical rule: If your token sale story is stronger than your current operating business, you’re probably fundraising too early.

Which source fits which founder

- Choose launchpads when your token utility is credible, your community is active, and you’re prepared for cross-border token distribution risk.

- Choose VC when your project still needs product depth, strategic partners, or a longer runway before public launch.

- Choose crowdfunding when you need a compliant local proof point, especially for Dubai-based operating businesses that may later add tokenised layers.

A founder deciding between these routes should also study how fundraising friction changes by stage, not just by platform. This breakdown of crypto startup funding challenges in Web3 is useful because it frames the bottlenecks that usually appear before a token sale, not after it.

The strongest UAE play is usually hybrid

This is the part most founders don’t reach on their own. In the UAE, the smartest fundraising architecture is often hybrid:

- local entity and compliance foundation first

- private or crowdfunding capital next

- token launch later, once jurisdictional controls and investor segmentation are mature

That sequence is slower than a pure offshore IDO. It’s also far more defensible.

The Top Crypto Fundraising Platforms for UAE Projects in 2026

The UAE offers founders something few markets do at the same time: regulatory momentum, deep regional capital, and a credible crypto user base. What it still does not offer is a mature, regulated local launchpad stack built for token issuance. That gap shapes platform selection more than brand recognition does.

For a UAE project, the main question is not which platform is best in isolation. It is which platform fits your capital stage, investor mix, and regulatory exposure. In practice, that creates four distinct categories: globally liquid exchanges, regional regulated venues, local non-token fundraising platforms, and offshore decentralised launchpads.

Binance

Binance remains the first name many founders assess because it combines exchange scale with licensed operations in Dubai. That makes it strategically relevant even when it is not your immediate fundraising venue.

The practical advantage is distribution depth. If your roadmap points toward exchange visibility, secondary market liquidity, and broad international reach, Binance becomes the benchmark against which other options are measured. It also carries a higher preparation threshold. Projects need stronger diligence, clearer token logic, and a more defensible market case than they would for a small community raise.

For UAE founders, Binance is less a default choice than a reference point. It defines the upper end of what exchange-led fundraising credibility looks like.

BitOasis and Rain

BitOasis and Rain are more useful as regional infrastructure than as pure fundraising engines. Founders often underrate that distinction.

These platforms matter when the objective is to build a credible Gulf operating and investor story before attempting wider token distribution. Their value comes from regional familiarity, fiat on-ramps, and a compliance posture that fits a founder who expects regulators, banking partners, or enterprise customers to examine the structure closely.

That makes them more relevant for projects building in payments, tokenised real-world assets, or enterprise Web3 than for teams chasing rapid retail token velocity.

DubaiNEXT

DubaiNEXT belongs on the shortlist for a different reason. It addresses a funding stage that many token-first founders try to skip.

A Dubai-based venture with a clear operating business can use a government-backed crowdfunding environment to test demand, sharpen its public narrative, and establish early capital formation without introducing token distribution risk too early. That is often the missing step between concept validation and any later crypto-native raise.

Founders planning a regulated or quasi-regulated product should take this route seriously. A compliant early round can improve later discussions with both private investors and digital asset partners.

Beehive and Wahed

Beehive and Wahed are not crypto fundraising platforms. They still matter in a UAE fundraising strategy because they show where compliant digital capital formation already works.

For the right company, especially one with a revenue model that extends beyond token speculation, platforms in this category can help establish investor confidence before any onchain fundraising begins. That signal is useful in the UAE, where credibility often depends on business fundamentals first and token mechanics second.

This is the broader strategic point. In the UAE, the strongest fundraising stack is often hybrid by design, not purely crypto-native from day one.

Global decentralised launchpads

Global launchpads across Solana, Ethereum, and BNB Chain remain relevant because local regulated token-sale infrastructure is still thin. For some UAE projects, they are the only realistic route to crypto-native community funding at scale.

Their usefulness comes with clear tradeoffs. Offshore launchpads can solve access, audience, and distribution. They do not solve local legal alignment. If your founders, entity, investors, or marketing operations are tied to Dubai or the wider UAE, an offshore IDO venue cannot be treated as a neutral wrapper around fundraising activity.

That is why platform choice should start with jurisdictional fit, not token sale mechanics. A technically successful launch can still create licensing, marketing, or investor eligibility problems later.

Global launchpads solve distribution. They do not solve jurisdiction design.

What Are the Best Platforms for Crypto Fundraising in the UAE?

The strongest answer is conditional.

- Best for exchange-led visibility and global reach: Binance

- Best for regional credibility and regulated market alignment: BitOasis and Rain

- Best for early non-token capital formation in Dubai: DubaiNEXT

- Best for hybrid digital finance pathways: Beehive and Wahed

- Best for crypto-native token distribution: selected global IDO launchpads, used only within a clear legal structure

Founders entering the UAE market should not treat these as interchangeable options. The smarter approach is sequencing. Start with the platform that fits your current regulatory and business reality, then add broader crypto distribution only when the structure can support it.

Navigating VARA Regulations for Compliant Fundraising in Dubai

The UAE is crypto-friendly, but that doesn’t mean every fundraising route is locally clean. Dubai’s regulatory framework has matured quickly, yet there’s still a practical mismatch between licensed virtual asset activity and founder demand for token-sale infrastructure.

The compliance gap founders run into

One of the clearest market gaps is this: VARA had licensed 16 platforms by Q1 2026, yet none were fundraising-focused, which leaves UAE projects looking to global IDO venues and dealing with the resulting non-compliance risk (Webopedia overview of UAE exchanges and licensing).

This has two implications. First, regulation in the UAE is ahead of local launchpad infrastructure. Second, founders can’t assume that because a market is pro-crypto, it already supports every crypto-native fundraising model inside a local regulatory wrapper.

What founders should do instead

Start with business design, not token design. That means defining:

- Entity footprint: Where the operating company sits, and which regulator has practical relevance.

- Investor access model: Whether you’re targeting accredited, institutional, retail, or mixed audiences.

- Marketing perimeter: Which jurisdictions you’ll actively solicit.

- Token function: Utility, governance, access, or security-like rights.

Those decisions determine whether your launch looks like a regulated capital raise with a token layer or an offshore token sale awkwardly attached to a UAE company.

Founders dealing with this should review a structured Web3 regulatory compliance framework before they build investor funnels, vesting contracts, or launch mechanics. Technical architecture and legal architecture have to be aligned from the start.

Where teams often make avoidable mistakes

The most common mistakes are operational, not ideological:

- Launching globally too early: Teams market internationally before defining which investors they can legitimately onboard.

- Copying offshore launchpads: They reuse templates designed for jurisdictions with very different enforcement expectations.

- Treating KYC as a plug-in: In practice, KYC and AML shape the entire investor journey and should influence product design.

- Ignoring sale sequencing: Private allocation, treasury policy, community sale, and exchange listing need to fit one coherent plan.

If your legal counsel and smart contract team are working from different assumptions, the fundraising strategy will eventually break.

A short explainer can help founders visualise the issue before they commit to platform selection.

The strategic conclusion

Dubai gives founders a better regulatory environment than most markets. But it still doesn’t offer a simple, domestically native answer for early-stage token fundraising. That’s why serious UAE projects tend to use staged structures, local-first compliance, and selective global execution rather than pretending one launchpad solves everything.

A Strategic Framework for Choosing Your Fundraising Platform

Platform selection is a capital strategy decision, not a distribution afterthought. In the UAE, that matters more than in many other markets because founders often face a structural gap. The jurisdiction is supportive of digital asset businesses, yet there is still no single domestically native, fully standardised path for early-stage token fundraising. As a result, the strongest fundraising plans are usually hybrid. They combine locally defensible entity, compliance, and investor onboarding choices with carefully selected global token distribution venues.

A useful starting point is sequence. Choose the fundraising route only after you are clear on business model, token function, and target investor profile, but before public campaign planning begins. If that order slips, teams end up selecting a venue that clashes with their actual capital needs, or worse, forces them into a sale structure that creates avoidable regulatory and operational strain.

Start with four questions

These questions help narrow the field quickly.

What stage is the company at?

A pre-product company raising to test demand needs a different channel from a protocol preparing for broad token distribution or secondary market activity.What does the token need to do?

If utility, governance rights, or economic function are still under debate, a private round or staged financing model is usually more defensible than rushing into a public token venue.Which investors should be admitted into this round?

Strategic backers, institutions, family offices, and retail community participants have different diligence expectations, allocation sizes, and onboarding requirements. One funnel rarely serves all of them well.How much structural complexity can the team realistically handle?

A global sale path may widen reach, but it also increases coordination across legal review, investor screening, smart contract design, treasury controls, and communications.

Match the platform to the real objective

Founders often compare fundraising platforms as if they were media channels. They are closer to operating systems. Each option shapes who can participate, how funds move, what disclosures are expected, and how hard the raise will be to defend later.

- If local defensibility matters most, begin with regulated, private, or institution-facing routes. Public token distribution can come later, once the structure and disclosures are more mature.

- If liquidity matters most, assess exchange-linked options based on listing standards, post-sale market support, and the quality of the investor base, not just audience size.

- If community formation matters most, use launchpads only after geographic restrictions, KYC logic, and token allocation rules are properly defined.

- If time for product development matters most, private capital often buys better execution room than a fast public raise with immediate market expectations.

Commercial discipline matters here too. Platform fees are only part of the cost. Founders should compare integration work, compliance overhead, investor support load, treasury operations, and the constraints a third-party venue may impose on future rounds. This guide to competitive intelligence pricing is useful because it sharpens platform comparison beyond feature lists and headline access.

A practical scoring model

A simple scorecard usually produces better decisions than intuition alone. Rate each route against the factors below:

| Decision factor | Low score means | High score means |

|---|---|---|

| Compliance fit | Hard to defend under your operating structure | Clean fit with entity, jurisdiction, and investor rules |

| Investor access | Audience is narrow or poorly matched | Strong fit with the specific buyers you want |

| Liquidity pathway | Limited support after the raise | Credible route to active trading and market continuity |

| Execution burden | Heavy custom work across teams | Operationally manageable for your current capacity |

| Brand trust | Investors need extra convincing | Venue already carries credibility with your target market |

One factor deserves extra weight in the UAE context: optionality. A platform that looks impressive on launch day can still be the wrong choice if it reduces your ability to adjust sale sequencing, tighten jurisdiction filters, or separate local fundraising from global token distribution later.

Operating principle: Choose the platform that lowers downstream friction across compliance, investor operations, treasury, and future rounds.

For UAE founders, that conclusion is often uncomfortable but useful. The strongest route is rarely the most visibly crypto-native. It is the route that lets you raise capital now without closing off better, cleaner distribution options later.

If you need a more detailed operating checklist before launch, use this founder checklist for 2026.

How Blocsys Builds Enterprise-Grade Crypto Fundraising Platforms

Some founders should use existing venues. Others need custom infrastructure because the fundraising process is part of the product itself. That’s especially true for exchanges, tokenised asset platforms, DTF structures, cross-chain products, and institutional fundraising environments.

When custom infrastructure makes sense

Custom build becomes rational when you need:

- Jurisdiction-aware onboarding rather than generic wallet connection

- Custom vesting and allocation logic tied to your tokenomics

- Integrated compliance workflows across KYC, AML, and investor approvals

- Treasury and distribution controls that fit institutional or multi-stage raises

- White-label investor experience instead of dependence on a third-party launch venue

In those cases, off-the-shelf launchpads can become a constraint rather than an accelerator.

A founder evaluating this path usually needs both product strategy and implementation capability. That’s where a Web3 consulting company and a dedicated IDO launchpad platform team become relevant, especially when the goal is to build fundraising infrastructure rather than merely participate in someone else’s ecosystem.

What founders should expect from a serious build partner

The bar is higher than “can they code smart contracts?” You need a team that can connect:

- token issuance logic

- investor onboarding

- sale mechanics

- compliance controls

- post-sale distribution

- admin and treasury operations

That’s the difference between a launch campaign and a fundraising system.

Blocsys works in that category. It builds production-ready blockchain and AI-powered platforms for digital asset businesses, including token launch infrastructure, trading systems, and compliance-aware workflows. For founders in the UAE, that matters when the objective isn’t just to raise once, but to build a repeatable capital formation capability.

If your team is choosing between adapting to someone else’s launchpad and building fundraising infrastructure that fits your operating model, talk to Blocsys before you commit to the wrong architecture.

Frequently Asked Questions about Crypto Fundraising in UAE

What are the best crypto fundraising platforms in UAE?

There is no single best platform because UAE fundraising usually spans two systems at once. Founders often need one channel for compliant local capital formation and another for global token distribution. In practice, exchange-linked venues such as Binance can matter for reach, while regional players such as BitOasis and Rain matter for market access and regulatory fit. For earlier-stage or non-token rounds, local crowdfunding and private capital routes can be more practical than forcing a token sale too early.

How do blockchain startups raise funds in Dubai?

The stronger approach is staged. A team sets up the right legal entity, raises initial capital through private investors, strategic partners, or compliant financing channels, then introduces a token sale only after investor onboarding, treasury controls, and token design are ready.

That sequencing matters in the UAE because the business environment is crypto-friendly, but locally regulated token launchpad infrastructure is still limited.

Is crypto fundraising legal in UAE?

It can be, but legality depends on structure. The key variables are where the entity is formed, which regulator has oversight, who the investors are, how the token is classified, and how the offering is marketed.

That means a token raise is not judged only by the asset itself. It is judged by the full operating model around it.

What is the best launchpad for crypto projects?

The best option depends on what problem the founder is trying to solve. Exchange-linked routes can help with credibility, distribution, and secondary market access. Decentralized launchpads can work for crypto-native communities, but they add more screening, jurisdiction, and compliance questions.

For UAE founders, launchpad selection should start with investor eligibility and regulatory exposure, then move to marketing reach.

How does token fundraising work?

A project sets token supply, pricing, allocations, vesting, access rules, and sale mechanics. Investors complete onboarding, commit capital, and receive tokens either at distribution or over a release schedule.

The operational challenge is usually not the sale page. It is connecting compliance checks, payment flows, cap table logic, and token distribution into one process.

What is the difference between ICO and IDO?

An ICO is run by the project through its own sale structure. An IDO is conducted through a decentralized launch venue.

The strategic difference is control versus distribution. ICOs give the issuer more control over the process. IDOs can improve market access and community participation, but they also create more complexity around investor filtering and jurisdictional fit.

Can startups raise crypto funding in Dubai legally?

Yes, if the structure is designed for Dubai rather than copied from another market. A model that works in a lightly regulated token sale jurisdiction may create problems in the UAE if investor access, disclosures, or token rights are not aligned with local expectations.

A staged raise is often the lower-risk path.

What are the top crypto launchpads in UAE?

The better question is whether a UAE founder needs a local launchpad at all. The UAE has built a strong digital asset base, but it still does not offer a deep bench of locally rooted, fundraising-specific token launch venues.

That gap is why hybrid models matter. Founders often use UAE-based entities and compliant investor processes for the local side, then use selected global platforms for token distribution and market reach.

Are there compliant alternatives to pure crypto launchpads in the UAE?

Yes. Some founders use regulated or lower-risk funding routes before introducing a token sale. That can include equity-style crowdfunding, private placements, revenue-based financing, or licensed exchange relationships, depending on the business model.

The strategic point is simple. In the UAE, fundraising infrastructure is often assembled rather than bought off the shelf. Founders who treat local compliance and global token access as two separate design problems usually make better platform decisions than teams searching for a single launchpad to do everything.

If you’re planning a token raise, an exchange-backed launch, or a hybrid fundraising model in Dubai, Blocsys Technologies can help design the infrastructure behind it. The team builds launchpad systems, token distribution workflows, trading infrastructure, and investor onboarding products for Web3 and digital asset businesses. If your goal is a fundraising stack built for your operating model rather than a generic template, Blocsys is one of the firms working in that category.