This guide is for banking leaders, fintech innovators, and Web3 founders evaluating how blockchain in banking is reshaping financial services. It defines core concepts, analyzes real-world use cases, and provides a decision framework for building production-grade platforms. By the end, you will understand the strategic and technical requirements needed to leverage this technology for a competitive advantage through 2026 and beyond.

What Is Blockchain in Banking?

Blockchain in banking refers to the use of a shared, immutable digital ledger (Distributed Ledger Technology or DLT) to record and verify financial transactions. Instead of each bank maintaining its own private, siloed ledger, participants on a blockchain network share a single, synchronized source of truth. This fundamentally changes how trust is established and value is exchanged, moving from a system reliant on intermediaries to one based on cryptographic certainty.

Think of a traditional banking system as a series of separate, private notebooks. For a transaction to clear, each institution must update its own notebook and then spend time and money reconciling all of them to ensure they match. It’s slow, costly, and prone to error.

Blockchain replaces those separate notebooks with a single, collaborative digital record. Once a transaction is added, it is cryptographically linked to the one before it, creating an unalterable chain. This builds immense trust and eliminates the constant need for reconciliation.

This shared ledger creates a single source of truth that is cryptographically secured, immutable, and transparent to all authorized participants. This isn’t just a technical upgrade; it’s a new operational paradigm that reorganizes how financial institutions collaborate and compete.

For decision-makers at both enterprises and startups, the outcomes are clear:

- Accelerated Settlement: Transactions clear in minutes or seconds, not days, by removing multiple layers of verification.

- Reduced Operational Costs: Smart contracts automate manual processes and eliminate intermediaries, cutting operational overhead.

- Enhanced Security and Trust: The immutable and transparent nature of the ledger drastically reduces the risk of fraud and data manipulation.

Traditional vs. Blockchain-Enabled Banking: A Comparison

The structural advantages of blockchain become clear when compared directly with legacy systems. For leaders evaluating investment, this framework highlights the key performance indicators (KPIs) that are most impacted.

| Feature | Traditional Banking System | Blockchain-Enabled System |

|---|---|---|

| Ledger System | Centralised and siloed; each bank maintains its own private ledger. | Decentralised and shared; all participants view a single, synchronised ledger. |

| Transaction Speed | Slow, often taking days (T+2) for settlement due to intermediaries. | Near real-time; settlement can occur in minutes or seconds. |

| Operational Costs | High due to intermediaries, reconciliation processes, and manual overhead. | Lower, as smart contracts automate processes and reduce the need for intermediaries. |

| Transparency | Opaque; limited visibility for external parties, requiring audits for trust. | High; all approved participants can view transactions, ensuring transparency. |

| Security | Vulnerable to single points of failure, fraud, and data breaches. | Highly secure due to cryptographic linking and decentralised nature; immutable records. |

| Reconciliation | Requires constant, complex reconciliation between different ledgers. | Minimal to no reconciliation needed as there is a single source of truth. |

This shift delivers a fundamental advantage in efficiency, cost, and resilience, creating a superior financial infrastructure. This is why global adoption is accelerating. For example, the market for blockchain in banking and financial services is projected to grow from $10.65 billion in 2025 to $16.27 billion in 2026—a massive compound annual growth rate (CAGR) of 52.8%.

This trend is driven by both incumbent banks seeking to modernize and fintech innovators building new financial products from the ground up. By exploring complementary technologies like AI-powered banking solutions, it becomes clear how these systems converge to unlock new efficiencies. For a deeper dive into building next-gen financial services, our guide on blockchain for fintech companies provides a valuable starting point.

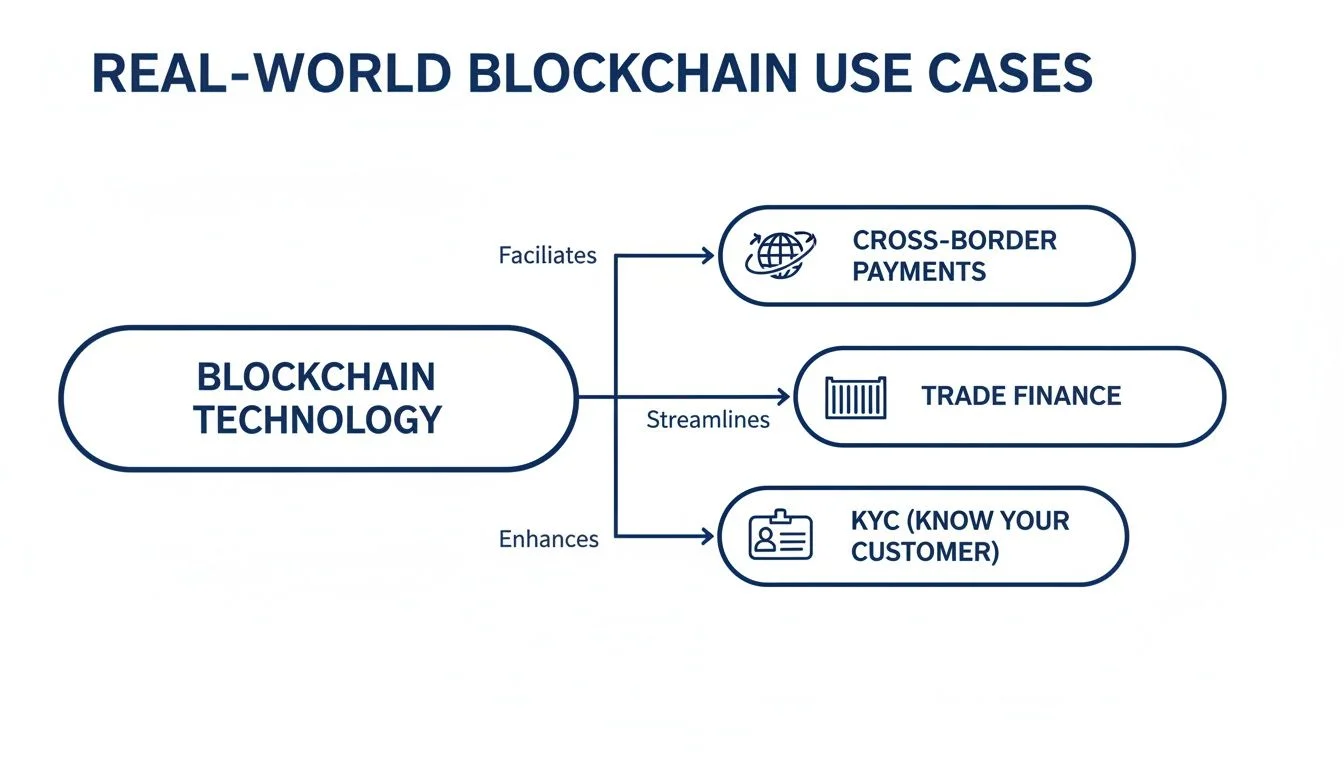

What Are the Key Use Cases for Blockchain in Banking?

Blockchain is no longer theoretical; it is actively solving long-standing problems in finance today, delivering proven ROI in speed, cost, and security. For decision-makers evaluating where to invest, these production-ready applications demonstrate the technology’s value across core banking functions.

Reinventing Cross-Border Payments

The legacy system for international payments is notoriously slow and expensive, routing funds through a complex web of correspondent banks. Each stop adds fees and delays, often holding up transactions for days and tying up capital.

Blockchain creates a more direct, peer-to-peer network where financial institutions can transfer value directly.

This streamlined process settles international payments in minutes, not days, and at a fraction of the cost. The result is unlocked liquidity for businesses and a vastly improved experience for consumers, solving a major friction point in global commerce.

Streamlining Trade Finance

Trade finance is burdened by paper-based processes—bills of lading, letters of credit, and invoices—that are inefficient and vulnerable to fraud. Blockchain digitizes this entire workflow by placing all documents on a shared, immutable ledger accessible to all authorized parties (importers, exporters, banks, shippers).

Smart contracts then automate key steps, triggering payments or releasing goods once predefined conditions are met. This has a dramatic impact. For instance, the India Trade Connect platform, a consortium of 15 major banks, is using blockchain to reduce processing times from days to hours and cut costs by up to 70%. Similarly, ICICI Bank’s TradeChain platform has successfully handled over $100 million in tokenized letters of credit with error rates below 1%. These results signal a clear trend, aligning with Asia-Pacific’s projected 73.8% CAGR in the blockchain BFSI sector.

Enhancing Identity Verification with KYC/AML

Know Your Customer (KYC) and Anti-Money Laundering (AML) compliance checks are critical but highly repetitive and costly. Each time a customer onboards with a new institution, the process starts from scratch.

Blockchain enables decentralized identity, where a customer creates a single, reusable digital identity verified by a trusted party. This ID can then be presented to other institutions without resubmitting sensitive documents.

- For Customers: It provides greater control over personal data and a seamless onboarding experience.

- For Banks: It dramatically reduces administrative overhead and costs associated with redundant KYC checks.

- For Regulators: It strengthens security and improves the ability to track and prevent illicit financial activity.

Unlocking New Markets with Asset Tokenization

Asset tokenization is arguably the most transformative use case. It is the process of converting ownership rights of a real-world asset (RWA)—like commercial real estate, fine art, or private equity—into a digital token on a blockchain. For a comprehensive overview, explore our complete guide on how real-world asset tokenisation works.

This makes historically illiquid assets divisible, accessible, and easily tradable. Instead of needing millions to invest in commercial property, individuals can buy fractional ownership via tokens. This democratizes access to exclusive asset classes, creates deeper market liquidity, and opens powerful new revenue streams for financial institutions.

How to Build a Technical Blockchain Framework

Transitioning from a strategic vision to a live platform requires making critical architectural decisions that will define your system’s performance, security, and scalability. These choices are foundational to your business model and user experience.

The first step is selecting the right consensus mechanism—the protocol nodes use to agree on the state of the ledger. This decision involves a crucial trade-off between speed, security, and decentralization.

A consensus mechanism is the set of rules a blockchain network uses to validate transactions and maintain a single, true version of the ledger. Your choice directly impacts transaction finality speed and the network’s resilience against attacks.

How to Choose a Consensus Mechanism for a Financial Platform?

For financial applications, two mechanisms are most prominent: Proof-of-Stake (PoS) and Practical Byzantine Fault Tolerance (PBFT).

- Proof-of-Stake (PoS): Participants stake their own crypto assets to validate transactions. It’s highly energy-efficient and scalable. However, public PoS networks can have longer finality times, which may be unsuitable for applications like high-frequency trading that demand immediate settlement.

- Practical Byzantine Fault Tolerance (PBFT): Designed for private or permissioned networks where participants are known and trusted, PBFT uses a voting system among a pre-approved group of nodes. It delivers extremely fast transaction speeds and instant finality but is more centralized. This makes it ideal for enterprise consortia but less suitable for open markets.

Your use case dictates the choice. A settlement platform for a closed group of banks would benefit from PBFT’s speed, while a public asset marketplace may require the greater decentralization of PoS. You can learn more in our guide to public versus private blockchain systems.

Which Custody and Wallet Infrastructure Is Right for You?

Once the consensus model is set, the next decision is how users will store and manage their assets. This involves custody solutions and wallet infrastructure.

Custody solutions determine how digital assets are secured. The primary options are self-custody (users control their private keys) or third-party custody (a trusted entity secures the assets). For institutional clients, a qualified third-party custodian is often a regulatory requirement, providing enterprise-grade security and insurance.

Wallet infrastructure is the user-facing software for managing funds. An intuitive and secure wallet is critical for adoption, whether it’s a mobile app for retail users or a multi-signature solution for corporate treasuries.

How to Choose Between an Order-Book and AMM for Trading?

If you are building a trading platform or decentralized exchange (DEX), you must choose between a traditional order-book model and an Automated Market Maker (AMM). This decision will define your target audience and competitive strategy.

This framework helps guide the choice based on your platform’s goals:

Decision Framework: Order-Book vs. AMM for Trading

| Consideration | Order-Book Model | Automated Market Maker (AMM) |

|---|---|---|

| Target User | Professional traders, market makers | Retail users, liquidity providers, passive investors |

| Liquidity Needs | Requires deep liquidity to avoid wide spreads | Can operate with very low liquidity |

| Price Discovery | Precise; based on specific buy/sell orders | Algorithmic; based on the ratio of assets in a pool |

| User Experience | Complex (limit/market orders, depth charts) | Simple (swap interface) |

| Best For | Liquid assets (e.g., major cryptos, stablecoins) | Long-tail or newly-listed assets with low volume |

| Key Risk | Market manipulation, low liquidity stalls trading | Slippage on large trades, impermanent loss for providers |

An order-book model mimics traditional exchanges by matching buy and sell orders, offering price precision favored by professional traders but requiring high liquidity. An AMM uses algorithms and liquidity pools to price assets, making it simpler for beginners and ideal for illiquid assets, but it can suffer from “slippage” on large trades.

Navigating Security and Regulatory Frameworks

In finance, security and regulatory compliance are non-negotiable. For any blockchain-based platform, they are the bedrock of trust required to win over both enterprises and fintech startups. This means building a fortress around the technology through robust security protocols, rigorous smart contract audits, and proactive defense against vulnerabilities like re-entrancy attacks and oracle manipulation.

Why Are Smart Contract Audits Essential for Security?

Smart contracts are the automated engines of blockchain applications, but a single coding flaw can lead to devastating financial losses. This makes comprehensive auditing a mandatory part of the development lifecycle.

A smart contract audit is an in-depth code review conducted by security experts to identify vulnerabilities, logical errors, and potential exploits. It is the equivalent of a team of locksmiths testing every mechanism of a bank vault before it is used to store valuables.

An effective audit is a multi-layered process that includes:

- Automated Scanning: Using specialized tools to detect common coding errors and vulnerabilities.

- Manual Code Review: Meticulous line-by-line inspection by experienced security engineers to find subtle flaws that automated tools miss.

- Penetration Testing: Simulating real-world attack scenarios to test the platform’s defenses under stress.

- Formal Verification: Using mathematical methods to prove that the code functions exactly as intended, the gold standard for high-value contracts.

Embedding this rigorous audit process ensures an enterprise-grade platform that is trustworthy from day one.

How to Prepare for Evolving Financial Regulations?

The regulatory landscape for digital assets is maturing rapidly. By 2026, financial institutions will face more defined requirements for Anti-Money Laundering (AML), Know Your Customer (KYC), and digital asset reporting. Regulators are no longer on the sidelines. For example, recent guidance from the U.S. Office of the Comptroller of the Currency (OCC) affirmed that national banks can engage in certain crypto-related activities, signaling a move toward more structured oversight.

This dynamic environment requires a forward-thinking, adaptable approach to compliance.

How to Build Intelligent Compliance Workflows?

The most effective solution is to embed compliance directly into the blockchain architecture, creating a powerful synergy between blockchain and AI. By integrating AI-driven tools, platforms can automate much of the regulatory workload.

These intelligent workflows can:

- Automate Reporting: Automatically generate and submit regulatory reports from on-chain data, reducing manual effort and human error.

- Monitor Transactions in Real-Time: Use AI algorithms to flag suspicious activity indicative of money laundering, enabling faster intervention.

- Streamline Onboarding: Integrate with decentralized identity solutions to make KYC processes more efficient and secure.

This automated approach transforms compliance from a reactive chore into a proactive, intelligent function, ensuring platforms remain compliant with evolving standards while lowering operational costs.

What Is the Future Outlook for Blockchain in Banking? (12-24 Months)

Looking ahead 12 to 24 months, the future of finance lies in the convergence of blockchain and Artificial Intelligence (AI). This powerful combination will unlock capabilities far beyond today’s foundational use cases, creating a new generation of intelligent, autonomous financial systems.

This convergence represents a shift from passive record-keeping to active, intelligent automation. Blockchain provides the secure, immutable foundation, while AI serves as the analytical brain, making data-driven decisions on top of that foundation.

Imagine AI-powered predictive analytics executing trades directly on decentralized finance (DeFi) platforms, optimizing strategies based on real-time on-chain data and risk parameters. This opens up new opportunities for Web3, crypto, and carbon tech companies to build entirely new, intelligent markets.

The Rise of Programmable Money and CBDCs

Central Bank Digital Currencies (CBDCs) are a major catalyst, integrating blockchain into a nation’s core financial infrastructure. The programmability of CBDCs will unleash a wave of financial innovation. For example, India’s e-Rupee pilot, launched in 2022, is on track to exceed 5 million users by late 2025 and has already processed over 100 million transactions. With 134 countries exploring CBDCs, this global trend is fueling rapid growth. The Asia-Pacific region alone is projected to see its blockchain banking market reach $16.27 billion by 2026 (a 52.8% CAGR), while AI adoption in finance is expected to rise from 37% in 2023 to 59% by 2026.

Programmable money allows for conditional payments, such as a government subsidy that can only be spent on specific goods or carbon credits released automatically once an AI-powered sensor verifies a reforestation milestone.

New Frontiers in Decentralized Markets

The fusion of AI and blockchain is paving the way for more sophisticated, high-value decentralized markets.

Next-generation platforms will include:

- AI-Optimized Carbon Trading: AI algorithms can analyze satellite and sensor data to verify carbon offset projects with unparalleled accuracy. These verified credits can then be tokenized and traded on a transparent blockchain marketplace, boosting liquidity and trust.

- Decentralized Equity Traded Funds (DTFs): These are funds governed by AI-driven smart contracts that automatically rebalance portfolios based on predefined market signals and risk tolerances, offering a transparent, low-cost alternative to traditional managed funds.

- Intelligent Prediction Markets: AI can aggregate vast data sets to provide more accurate odds and insights for markets forecasting financial, political, or other outcomes. Platforms like CoinStats AI offer a glimpse into the broader applications of AI within the blockchain ecosystem.

For founders in the Web3 space, the opportunity is clear: build platforms that are not just decentralized, but also intelligent.

How Blocsys Can Help You Build Your Blockchain Banking Platform

Building a production-grade blockchain banking platform—whether for trading, tokenization, or compliance—is more than a technical task. It requires a partner with deep expertise in the convergence of finance, technology, and regulation. The insights in this guide outline a clear path for fintechs, exchanges, and digital asset businesses ready to execute.

From selecting the right consensus model to architecting custody solutions and choosing between an order-book or AMM, every decision impacts scalability, security, and user adoption.

Expert guidance turns a powerful idea into an enterprise-grade reality. A strategic partner helps you navigate critical architectural decisions, avoid common setbacks, and significantly reduce your time-to-market by building on a secure and scalable foundation.

From Blueprint to Launch with Blocsys

For fintech innovators and digital asset pioneers, launching a production-ready platform is a specialized discipline demanding expertise in both blockchain and AI. Blocsys provides flexible development models tailored to your exact needs.

This collaboration can take two primary forms:

- End-to-End Development: For organizations needing a complete, custom solution, our team manages the entire lifecycle—from strategy and architecture to development, testing, and deployment.

- Staff Augmentation: For teams needing specialized skills, we provide expert blockchain and AI developers who integrate seamlessly into your existing workflows to accelerate progress.

Whether you’re building a decentralized trading platform, launching a real-world asset tokenization system, or creating intelligent compliance tools, we ensure your project is built on industry-leading practices.

Why Partner with Blocsys Technologies?

The financial technology landscape moves at an incredible pace. For businesses in the Web3, crypto, and carbon sectors, the ability to build and iterate quickly without compromising security is what defines market leaders. A dedicated partner like Blocsys Technologies offers the focused expertise needed to thrive in this environment.

We specialize in designing and building the secure, scalable, and enterprise-grade systems discussed in this guide, including tokenization frameworks, high-performance trading infrastructure, and AI-powered compliance workflows.

If you are ready to transform your vision into a market-leading financial platform, our experts are here to help you build, scale, and execute with confidence.

Connect with Blocsys today for a consultation and discover how we can help you build the future of finance.

FAQ: Blockchain in Banking

Here are answers to some of the most common questions we receive from consumers, banks, and fintech startups navigating the intersection of blockchain and banking.

What is the biggest advantage of blockchain in banking for a consumer?

The biggest consumer advantages are significantly lower costs and faster transaction speeds, particularly for international payments. Legacy systems use a chain of intermediaries, each adding fees and delays. Blockchain enables direct, peer-to-peer transfers that settle in minutes for a fraction of the cost. It also enhances security by recording asset ownership on an immutable ledger, making fraud much more difficult.

Should a bank use a public or a private blockchain?

Currently, most financial institutions are building on private, permissioned blockchains. Unlike public networks like Bitcoin where anyone can participate, a private blockchain restricts access to a vetted group, such as a consortium of trusted banks.

A private blockchain provides the efficiency and security of DLT while maintaining the data privacy and control necessary for regulatory compliance and high-speed processing. This model offers the best of both worlds: genuine blockchain benefits within a secure, enterprise-ready framework.

How can a fintech startup begin implementing blockchain?

A fintech startup should start by identifying a single, high-impact problem where blockchain offers a clear advantage over existing solutions, such as streamlining cross-border payments or simplifying trade finance. The next step is to build a Proof of Concept (PoC) to validate the technical approach and business case. Following a successful PoC, the focus should shift to developing a minimal viable product (MVP) that solves a core user need.

Partnering with an expert development firm can dramatically accelerate this process, ensuring the platform’s architecture is secure, scalable, and compliant from day one.

At Blocsys Technologies, we specialize in helping fintechs, exchanges, and digital asset businesses build these exact production-ready platforms. Our team designs tokenisation systems, trading infrastructure, and intelligent compliance workflows built for secure, scalable, and enterprise-grade operations. If you are ready to build the next generation of financial solutions, we have the expertise to get you there.

Start building your platform with Blocsys Technologies today.