Identity verification has moved from back-office compliance to product infrastructure. In India alone, the e-KYC market is valued at $450 million in 2025 and is projected to reach $1.2 billion by 2030 at a 22% CAGR, driven by regulatory mandates, mobile-first onboarding, and financial inclusion programmes, according to Facts & Factors coverage cited here. That shift matters far beyond one market. It signals what founders, compliance leaders, and product teams across the USA, UK, Europe, Singapore, Germany, and the UAE already feel in practice: KYC now shapes conversion, fraud exposure, and regulatory resilience at the same time.

For fintechs, crypto exchanges, AI-native platforms, and digital asset businesses, choosing among kyc verification companies isn’t a simple vendor shortlist exercise. The key question is whether a platform can verify users quickly, support regional compliance, integrate into your stack, and still adapt when your model expands into new products or jurisdictions.

Teams evaluating providers also need the discipline of operational due diligence. KYC doesn’t live in isolation. It touches onboarding policy, data governance, fraud controls, and escalation workflows. For organisations building decentralised systems, identity architecture matters just as much as verification tooling, especially where decentralised data security and digital identity design intersect with compliance.

The Critical Role of KYC in a Global Digital Economy

A modern KYC stack decides who gets through the front door of your platform. If that decision is too loose, fraud enters. If it’s too strict, legitimate users abandon onboarding. The strongest kyc service providers reduce that trade-off rather than forcing you to pick one side.

Global businesses now operate in a market where customer acquisition is digital, cross-border, and immediate. A bank in London, a payments platform in Singapore, a crypto venue in Dubai, and an AI product with users in Germany all face the same structural problem. They need to establish trust remotely, often before any human employee speaks to the customer.

Why KYC has become a growth control point

KYC used to be treated as a compliance gate placed after product strategy. That approach no longer works. The onboarding flow is now part of the product itself, and every additional verification step affects activation, support workload, and fraud review queues.

Three dynamics explain the change:

- Regulatory expansion: Rules increasingly apply to digital-first platforms, not just traditional banks.

- Fraud sophistication: Synthetic identities, document manipulation, and deepfake-assisted attacks have raised the technical bar.

- Global customer expectation: Users expect account opening to feel instant, especially in fintech and consumer trading products.

Practical rule: Treat KYC as a revenue-critical workflow. Procurement, compliance, fraud, product, and engineering should all score vendors together.

What decision-makers need from a global guide

Enterprise buyers and startup founders rarely need another generic feature list. They need a way to distinguish identity verification companies that look similar in a sales deck but behave very differently in production.

That distinction usually comes down to four realities:

- Coverage reality: Which regions, document types, and business entities does the provider support well?

- Integration reality: How much custom engineering will your team carry after contract signature?

- Policy reality: Can your compliance team configure rules without creating constant developer dependency?

- Data reality: Where is user data processed and stored, and how will that affect cross-border operations?

The companies that matter in 2026 aren’t only those with strong biometrics or broad marketing claims. They are the platforms that can support identity, business verification, AML controls, and long-term monitoring without creating friction your team can’t operationalise.

Understanding Core KYC and AML Compliance Principles

KYC is a digital handshake with evidence. AML is what happens after that handshake, when the platform keeps checking whether the relationship still looks legitimate. Businesses that separate the two too sharply usually create gaps. They verify identity once, then fail to monitor risk over time.

Customer identification is the first control

Most online kyc verification services start with the core question: is this person or business who they claim to be? In practice, platforms answer that through some combination of document capture, biometric checks, database matching, sanctions screening, and fraud signals such as device or behavioural anomalies.

This initial layer is commonly organised around Customer Identification Program, or CIP. The objective isn’t administrative completeness. It’s establishing a reliable identity baseline before access, payments, trading, or account functionality expands.

A strong CIP process usually includes:

- Document verification: Confirming the authenticity and integrity of passports, licences, national IDs, or local equivalents.

- Face matching and liveness: Checking that the user is present and matches the identity document.

- Basic sanctions and watchlist checks: Screening against restricted or politically exposed persons lists where required.

Due diligence determines risk depth

After identity comes Customer Due Diligence, or CDD. Here, many buyers underestimate vendor quality. It’s one thing to verify an individual. It’s another to decide whether that individual, entity, or ownership structure creates increased risk.

CDD becomes more involved when the customer is a business, a high-risk jurisdiction user, or a participant in complex financial activity. In those cases, teams often need enhanced checks on beneficial ownership, source of funds, or ongoing adverse media exposure.

A fast verification result isn’t enough. The important question is whether the result supports a defensible compliance decision.

Ongoing monitoring is where AML actually lives

AML compliance companies differ most clearly after onboarding. Static verification catches identity fraud at entry. Ongoing monitoring helps detect account misuse, shell entities, sanctions exposure, and patterns that emerge later.

That monitoring can include:

- Transaction review tied to suspicious behaviours or thresholds.

- Rescreening against updated PEP, sanctions, and risk databases.

- Profile refreshes when customer data changes or regulatory triggers apply.

For fintech and crypto operators, this matters because risk doesn’t stay still. A low-risk user at onboarding can become a high-risk user later, especially in products involving transfers, trading, or rapid account scaling. The best aml kyc providers support both the initial identity event and the surveillance logic that follows.

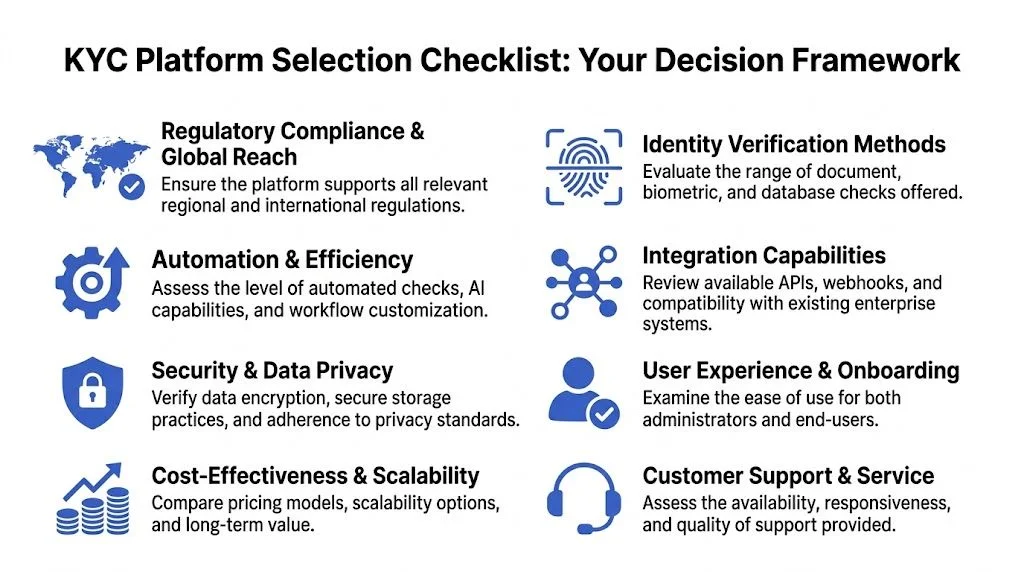

How to Choose a KYC Platform A Decision Framework

The fastest way to buy the wrong KYC platform is to compare vendors only on documents supported, liveness, and price. Those features matter, but they don’t explain whether the provider will hold up inside your onboarding funnel, compliance stack, and engineering roadmap.

A useful evaluation framework has to test platform fit under real operating conditions.

Evaluate technical fit before commercial fit

A vendor can look strong in a demo and still create months of implementation drag. Engineering teams should inspect the API model, SDK maturity, webhook design, fallback handling, and whether the provider supports modular deployment or forces a rigid hosted flow.

If your product spans mobile apps, embedded onboarding, or partner channels, this gets more important. The best identity verification API setups let teams control user experience while still capturing the evidence compliance teams require.

Use this scorecard early:

- Integration model: API-first, SDK-led, hosted workflow, or hybrid.

- Workflow flexibility: Can you create separate paths for retail users, high-risk geographies, and KYB?

- Operational controls: Can compliance teams adjust rules without requiring code changes for every policy update?

For teams comparing compliance tooling across functions, this wider stack perspective often overlaps with adjacent legal operations categories such as the best legal tech tools, especially where auditability and policy governance matter.

A short walkthrough helps surface what to test in demos and pilots:

Measure verification quality in context

Verification quality isn’t just an abstract accuracy score. It affects conversion, fraud leakage, and support burden. Regional depth also matters. A provider that performs well on passports in Europe may perform less well on local IDs in emerging markets or on complex business structures.

A concrete example comes from India. AU10TIX reports 98.7% verification accuracy for Aadhaar-based authentications, processes over 5 million monthly transactions for fintechs such as Paytm and PhonePe, and delivers 4 to 8 second response times. The same review states that those response times reduce onboarding drop-off by 45%, while passive facial biometrics counter 92% of synthetic fraud attempts in that context, according to AU10TIX’s 2026 KYC review.

That data matters because it reveals a broader evaluation principle. You shouldn’t ask only whether a vendor supports a region. Ask whether it performs strongly on that region’s real documents, regulatory flows, and fraud patterns.

Prioritise policy control and privacy readiness

Compliance teams often discover too late that a provider’s rule system is too coarse. If you operate in banking, lending, crypto, carbon markets, or tokenisation, you’ll likely need route-specific logic. Retail onboarding might be one flow. High-risk geographies, business onboarding, and politically exposed users need others.

Assess whether the vendor supports:

- Granular rule orchestration for risk-based onboarding

- Case management for manual review and escalation

- Data residency options where local privacy rules require in-region storage

- Audit trails that compliance teams can export and defend

Buyers often overvalue headline features and undervalue governance. The provider that gives your team policy control usually becomes more valuable than the provider with the flashiest demo.

Match the platform to your business model

The final screen is strategic fit. A payments app, a crypto exchange, and a B2B treasury platform don’t need the same stack shape.

| Business model | What matters most |

|---|---|

| Consumer fintech | Fast pass rates, mobile UX, scalable manual review fallbacks |

| Crypto exchange | Sanctions screening, source-of-risk monitoring, adaptable jurisdiction rules |

| B2B platform | KYB depth, UBO checks, registry coverage, audit logs |

| Marketplace or AI platform | Remote identity proofing, fraud controls, reusable workflows |

The strongest procurement outcome comes from separating core needs from edge cases. Then test whether the vendor can support both without pushing custom work back onto your team.

Navigating Global and Regional KYC Regulations

Regulation doesn’t create a single global KYC standard. It creates a patchwork of overlapping obligations. That matters because many kyc solutions providers market themselves as global while relying on a narrow operational model that only works smoothly in a handful of jurisdictions.

Europe and the UK focus on both AML and privacy

For operators in Europe and the UK, identity verification is never only about AML controls. It also sits inside strict privacy expectations. That combination shapes platform choice. Providers need strong evidence capture, retention discipline, and controllable data flows.

In practical terms, buyers in these markets usually evaluate:

- How personal data is stored and accessed

- Whether the provider supports explainable review paths

- How quickly screening rules can be adapted when regulation changes

- Whether business verification and beneficial ownership checks are sufficient for regulated financial services

For cross-border firms, the operational challenge is not just passing KYC. It’s aligning customer onboarding with privacy governance from day one.

The USA, Singapore, and the UAE tend to push operational readiness

The USA remains heavily focused on AML enforcement and traceability. Singapore places a premium on disciplined controls and regulatory clarity. The UAE has become a major venue for digital asset businesses, but firms still need a defensible compliance framework rather than a lightweight onboarding layer.

This means buyers in those regions should put pressure on vendors around:

- Screening coverage and alert management

- Case handling for escalations and suspicious activity review

- Support for both individual and business onboarding

- Ability to integrate KYC with broader transaction and risk systems

For Web3 and digital asset operators, policy orchestration matters as much as document checks. That’s one reason firms building cross-jurisdiction products often need a Web3 regulatory compliance framework that connects identity, screening, and operational controls instead of treating them as separate tools.

India shows why localisation is now a strategic issue

India illustrates a trend that global buyers shouldn’t ignore. After enforcement of the DPDP Act 2023 became effective in January 2026, 72% of Indian fintechs using providers such as Jumio and Veriff faced data localisation fines averaging ₹5-10 crore due to offshore storage. The same analysis states that only 15% of top platforms offer India-specific data residency, and stricter consent requirements led to a 25% drop in verification success rates for Aadhaar-linked checks. It also notes that localised providers such as Shufti Pro reduced compliance costs by 35% for carbon tech and prediction market firms, according to this 2026 review of KYC provider trends.

That finding changes the usual global-vendor narrative. Bigger isn’t automatically safer. In some markets, a regionally adapted provider or hybrid stack may outperform a well-known international platform because compliance depends on data location, consent handling, and local verification rails.

Regulation is no longer just a legal filter on top of technology. In many markets, it changes which technology architecture is viable at all.

Top Global KYC Verification Platform Companies A Detailed Review

The KYC market is fragmented for a reason. A provider that performs well for consumer fintech in Europe can struggle with Aadhaar-linked onboarding in India, beneficial ownership checks for complex entities, or wallet-linked risk controls for crypto products. For Web3, AI, and cross-border platforms, vendor selection is less about headline feature parity and more about how well a system fits the operating model, data residency requirements, and enforcement exposure of the business.

A useful shortlist starts with architecture, not brand recognition.

Comparison of Top KYC Platforms 2026

| Provider | Ideal For | Biometric Liveness | AI Fraud Detection | Global Coverage |

|---|---|---|---|---|

| AU10TIX | High-scale fintech and digital onboarding | Yes | Yes | Broad international coverage |

| Sumsub | Crypto, fintech, KYB-heavy operations | Yes | Yes | Broad international coverage |

| Signzy | India-first fintech and regulated onboarding | Yes | Yes | 190+ countries |

| Binderr | End-to-end KYC, KYB, AML screening and ongoing monitoring | Yes | Yes | 230+ countries and |

| Trulioo | Global database-led verification and KYB | Mixed by workflow | Yes | Broad international coverage |

| Onfido | Consumer onboarding with biometric emphasis | Yes | Yes | Broad international coverage |

| Jumio | Enterprise identity proofing and AML workflows | Yes | Yes | Broad international coverage |

| Veriff | Conversion-focused remote identity checks | Yes | Yes | Broad international coverage |

| Shufti Pro | Localisation-sensitive and cross-border use cases | Yes | Yes | Broad international coverage |

| Persona | Configurable identity infrastructure | Yes | Yes | Global business use |

| iDenfy | Mid-market fintech and fraud-led onboarding | Yes | Yes | International |

| KYC-Chain | Compliance-led workflows with blockchain orientation | Workflow dependent | Yes | Multi-jurisdictional |

| Refinitiv | Large enterprise risk and compliance teams | Limited onboarding biometrics focus | Yes | Global enterprise reach |

The table above is useful, but it hides an important distinction. Some vendors are strongest at first-pass identity verification. Others are better at orchestration, entity resolution, ongoing monitoring, or region-specific compliance rails. Crypto exchanges, AI marketplaces, prediction platforms, and tokenised asset businesses usually need more than document capture and face match. They need policy control across wallets, entities, sanctions, and jurisdictional routing, often through APIs that can be embedded into a broader blockchain-based identity verification for secure access stack.

AU10TIX

AU10TIX fits organisations that care about automated onboarding at scale and low manual review rates. It is often considered by businesses where fraud pressure is high and identity checks need to sit directly inside product flows rather than in a separate back-office tool.

Key features

- Automated identity verification: Designed for document and biometric checks in digital onboarding.

- Fraud analysis: Positioned around synthetic identity detection and risk scoring.

- Developer integration: Well suited to API-led product environments.

Ideal use cases

- Consumer fintech

- Trading platforms

- High-volume mobile onboarding

Global presence

- Commonly described in market reviews as a global provider with broad document and country support.

Sumsub

Sumsub is frequently shortlisted by teams that want KYC, KYB, AML screening, and monitoring in one control layer. That matters for crypto exchanges, B2B fintech infrastructure providers, and AI platforms handling both individuals and business counterparties. Its value is usually in workflow configurability and operational breadth rather than one standout verification method.

Key features

- Modular KYC and KYB: Supports individual and business verification flows.

- No-code orchestration: Lets compliance teams adjust policies without a front-end rebuild.

- Monitoring orientation: Better aligned than some peers with ongoing compliance operations.

Ideal use cases

- Crypto exchanges

- Multi-jurisdiction fintechs

- Platforms with complex business customers

Global presence

- Used internationally across fintech, crypto, and digital platforms.

A regional signal is relevant here. Sumsub reports a 99.2% pass rate for Indian KYB verifications on UBO structures, screens 2.3 million entities quarterly against MCA registries and PEP lists, and delivers 3-second fraud detection that cuts false positives by 67% compared with legacy systems. The same analysis says its graph database links 500+ regional data sources and flags 78% more shell company risks in crypto exchanges according to this KYC tools review.

For Web3 buyers, that combination matters because entity verification and transaction risk rarely sit in isolation. A provider that handles UBO complexity well can reduce the need for custom compliance stitching later.

Signzy

Signzy is strongest where Indian identity rails shape onboarding economics. That makes it relevant not only to domestic fintechs, but also to crypto and AI companies entering India and discovering that local document logic, consent flows, and registry connections affect approval rates more than generic global coverage claims.

Key features

- No-code workflow design: Useful for compliance-led implementations.

- Deep local integrations: Aligned with Indian identity and financial data sources.

- Fraud prevention tooling: Includes OCR, document intelligence, and deepfake-related controls.

Ideal use cases

- India market entry

- Regulated fintech onboarding

- Digital lending and UPI-adjacent products

Global presence

- Signzy says it can handle up to 1 million API queries per hour across 190+ countries, supports 150+ local data source integrations, covers 99% of Indian identity documents, and achieves 98.5% pass rates for Aadhaar-XML based verifications. The company also says its workflows reduce manual reviews by 85%, serves 500+ Indian clients, works with 30% of new-age banks, is projected to reach 2 billion cumulative verifications by the end of 2026, and has 99.7% OCR accuracy on PAN-Aadhaar combos, according to Signzy’s provider overview.

The strategic implication is straightforward. If India is a priority market, local rails can matter more than a longer international vendor list.

Binderr

Binderr is built for businesses that need more than a standalone identity check. It combines biometric identity verification with KYC, KYB, sanctions and PEP screening, adverse media, ownership mapping, risk assessment and ongoing monitoring in one compliance platform. Its identity verification workflow includes AI-powered document checks, OCR data extraction, biometric face matching, liveness detection and deepfake prevention. For business onboarding, Binderr can also verify company information, identify directors and beneficial owners, map complex ownership structures and continuously monitor customers and entities for changes in risk. This makes it particularly useful for regulated businesses that want to manage the full compliance lifecycle—from initial verification and screening to approval, audit trails and continuous monitoring—without connecting multiple separate tools.

Key features:

– Identity verification: Automated document verification, biometric face matching, liveness detection and deepfake prevention.

– Integrated KYC and AML: Sanctions, PEP, watchlist and adverse-media screening within the onboarding workflow.

– Business verification: KYB checks, registry data, UBO identification and corporate ownership mapping.

– Ongoing monitoring: Continuous screening and alerts when a customer, company or risk profile changes.

– Flexible implementation: Available through a central compliance dashboard, hosted onboarding flows and API integrations.

Ideal use cases:

– Corporate service providers

– Fintechs and payment companies

– Banks and electronic money institutions

– Law and accounting firms

– Crypto and other regulated businesses

Global presence: Binderr supports identity verification across more than 230 countries and over 11,000 identity-document types, alongside international KYC, KYB and AML screening workflows.

Trulioo

Trulioo is commonly evaluated by companies expanding across many jurisdictions at once. Its strength is broad data access and database-led verification, which can be useful where coverage breadth matters more than custom local document flows.

Key features

- Global data access: Supports wide coverage strategies.

- Identity and business verification: Handles both KYC and KYB use cases.

- Cross-border focus: Helpful for international expansion.

Ideal use cases

- Marketplaces

- Cross-border fintech

- Multi-region onboarding teams

Global presence

- Broadly recognised for verification support across numerous jurisdictions.

For crypto and AI platforms, Trulioo can be useful during early international expansion. The tradeoff is that some businesses will still need separate tooling for wallet screening, transaction monitoring, or more specialised local compliance logic.

Onfido

Onfido remains relevant for teams that put user experience and biometric onboarding quality near the top of the requirements list. It is often selected by product-led businesses trying to reduce onboarding friction without weakening identity assurance.

Key features

- Biometric verification: Focused on document plus facial authentication workflows.

- Consumer-friendly UX: Often chosen for polished onboarding.

- AI-backed checks: Supports automated decisioning in identity flows.

Ideal use cases

- Consumer apps

- Neobanks

- Regulated digital platforms with mobile-first onboarding

Global presence

- Operates internationally and is frequently evaluated in Europe, the UK, and North America.

Its limitation for more complex compliance environments is scope. Web3 and B2B2B platforms often need broader policy orchestration than biometric onboarding alone can provide.

Jumio

Jumio remains an established enterprise option for firms that want identity proofing and AML support within the same procurement process. It generally fits organisations with formal risk review and security assessment procedures.

Key features

- Identity proofing plus AML screening

- Biometric authentication

- Enterprise compliance workflows

Ideal use cases

- Larger regulated businesses

- Insurance and financial services

- Companies with stringent internal controls

Global presence

- Broad international footprint across regulated industries.

Jumio is often a safer fit for mature enterprises than for crypto-native teams building around wallets, smart contracts, and rapid policy iteration.

Veriff

Veriff is often selected when completion rates, verification speed, and remote identity checks need to work together. It tends to appeal to growth-stage digital businesses where abandoned onboarding has a direct revenue cost.

Key features

- AI-powered identity verification

- Liveness and face match checks

- Remote onboarding support

Ideal use cases

- Online platforms with rapid user acquisition

- Cross-border digital services

- Mobile-heavy onboarding funnels

Global presence

- International support across a wide range of digital businesses.

For AI consumer products and mainstream fintech apps, that can be a strong fit. For high-risk crypto products, Veriff is more often one layer in the compliance stack than the whole stack.

Shufti Pro

Shufti Pro is most relevant where localisation, broad language support, and flexible deployment requirements affect vendor selection. That makes it more interesting than its market visibility alone might suggest, especially for firms entering regions with tighter data handling rules.

Key features

- Real-time verification

- KYC, AML, and KYB support

- AI-assisted identity checks

Ideal use cases

- Cross-border services

- Carbon tech and regulated niche platforms

- Firms needing localisation-sensitive deployments

Global presence

- Broad international availability with adaptable compliance workflows.

For buyers dealing with residency constraints or country-specific workflow changes, Shufti Pro can be more practical than larger brands that offer wider coverage but less regional tuning.

Persona

Persona is better understood as identity infrastructure than as a packaged KYC product. That distinction matters for teams building multi-role systems, layered verification paths, or products where identity controls have to change by user type, jurisdiction, or transaction threshold.

Key features

- Modular identity components

- Configurable workflows

- Developer-oriented architecture

Ideal use cases

- Product teams building custom onboarding journeys

- Platforms with multiple user roles

- Enterprises needing identity orchestration

Global presence

- Used globally for flexible identity and verification design.

Persona is often a strong fit for AI and platform companies that need to design around dynamic trust tiers rather than a single onboarding funnel.

iDenfy, KYC-Chain, Refinitiv and others

Several vendors matter because they solve narrower problems well.

- iDenfy: Often suitable for mid-market fintech teams that want document verification, biometrics, and fraud checks without a large enterprise deployment.

- KYC-Chain: Relevant for teams that need blockchain-aware compliance workflows and multi-jurisdiction policy design.

- Refinitiv: Better aligned with institutions that treat KYC as part of a broader risk intelligence and screening environment.

- Didit and Ondato: Increasingly visible where pricing structure, workflow flexibility, or all-in-one compliance management influence the shortlist.

- IDology: More relevant for businesses with a North American focus and layered fraud controls.

The strongest shortlist is usually the one that reduces future integration debt. For a neobank, that may mean conversion-focused onboarding and broad document support. For a crypto exchange, it may mean KYB depth, sanctions screening, and policy hooks for wallets and transaction monitoring. For an AI platform handling users, agents, and business customers in multiple jurisdictions, the best choice is often the provider that gives compliance teams direct control over workflow logic rather than the vendor with the longest feature list.

KYC for Web3 Solving the Unique Compliance Puzzle

Traditional KYC assumes a familiar onboarding model. A person presents identity evidence, a platform verifies it, and the account sits inside a centrally controlled product environment. Web3 doesn’t work that neatly. Users interact through wallets, protocols, DAOs, cross-chain assets, and smart contracts that don’t map cleanly to old compliance patterns.

That mismatch explains why many crypto teams feel over-served by generic vendor lists and under-served in implementation.

Why Web3 breaks standard KYC assumptions

Most mainstream providers verify people and businesses well enough. The harder question is whether they support on-chain context. Wallet screening, transaction provenance, jurisdiction routing, and smart contract linked permissions often sit outside the native capability set of traditional identity verification companies.

A sharp example comes from India. Registered virtual asset service providers grew by 41% from March 2025 to March 2026 under PMLA compliance, yet providers such as Sumsub and Trulioo still lack native Web3 wallet verification for addresses like Ethereum or Polygon. A 2026 NASSCOM blockchain compliance survey of 150 Indian fintechs reported that custom API bridges increased latency by 30% to 50% and costs by 20%, while 68% of startups cited poor blockchain interoperability in provider evaluations, according to this 2026 KYC provider comparison.

That finding has two implications. First, KYC for crypto isn’t only about identity. Second, the integration layer becomes a strategic differentiator.

What Web3 teams should demand from a KYC stack

Crypto kyc verification platforms need more than liveness and sanctions checks. They need to fit an architecture where on-chain behaviour and off-chain identity sometimes have to be linked without breaking user flows.

The practical requirements usually include:

- Wallet-aware controls: Screening addresses and connecting them to onboarding policy where relevant.

- Flexible access logic: Applying different verification thresholds by product, token type, jurisdiction, or transaction context.

- Composable infrastructure: Letting teams connect identity, KYB, AML, and on-chain analytics into one operating model.

For firms building exchanges, tokenisation systems, prediction markets, or decentralised trading infrastructure, that often means pairing a provider with specialist implementation support such as blockchain-based identity verification for secure access, plus product-specific engineering for crypto trading platform development, prediction market platforms, or OTC trading systems.

In Web3, compliance architecture is part of product architecture. If your KYC layer can’t speak to wallet logic, your team will build the missing pieces itself.

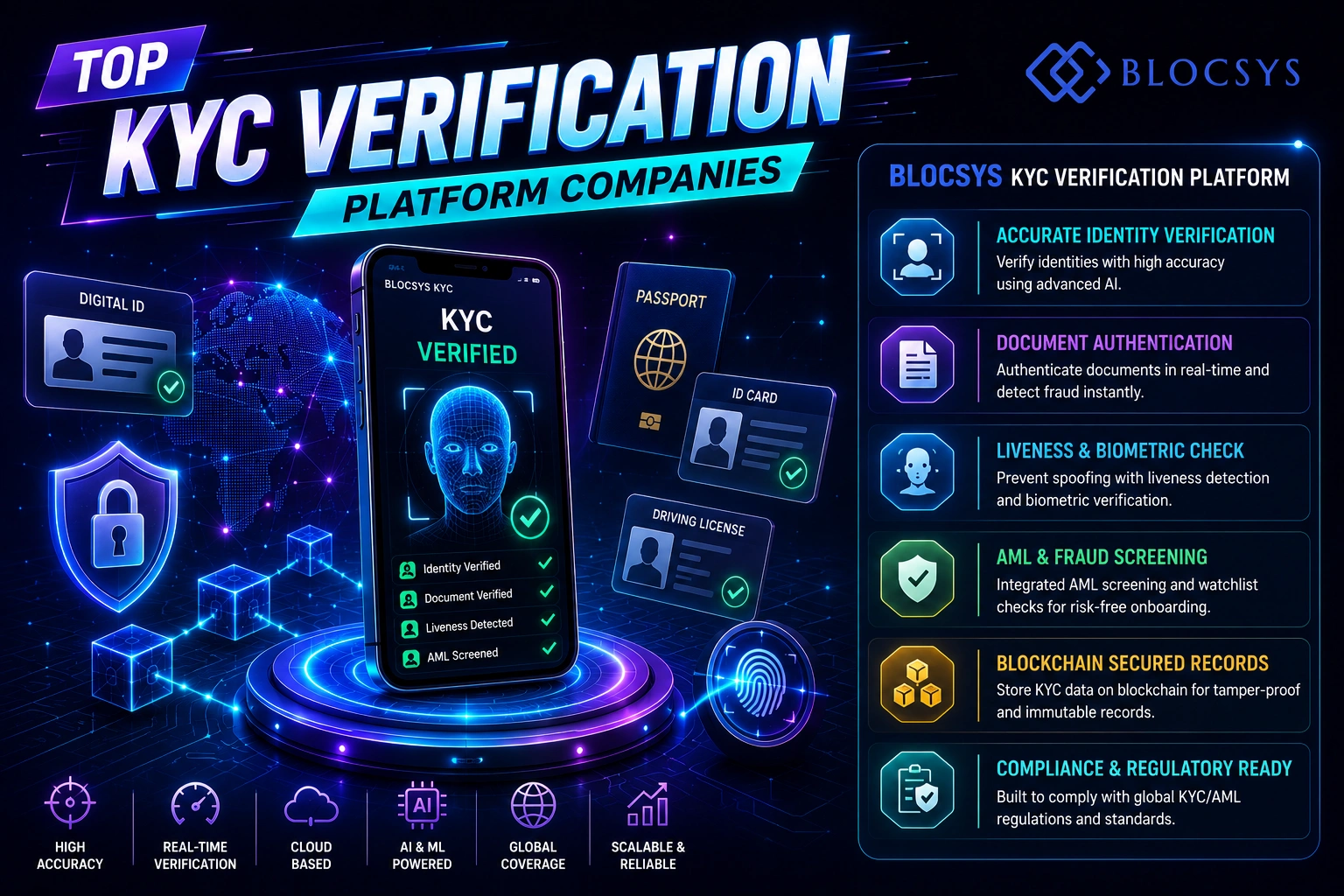

Building Compliant Platforms with Blocsys

Most KYC failures in Web3 products do not start with weak document checks. They start at the integration layer, where policy, identity, wallet activity, and transaction controls fail to stay in sync across the product stack.

That problem matters more for crypto, tokenisation, and AI platforms than for standard fintech apps. A regulated exchange, agentic trading product, or tokenised asset venue may need to apply one set of controls at onboarding, another at deposit or wallet connection, and a third when user behaviour changes. The operational question is not only which kyc software provider to buy. It is how verification outcomes flow into permissions, monitoring, case management, and audit records without creating brittle workarounds.

Blocsys Technologies is positioned in that implementation gap. It is not a KYC vendor. It works as a development partner for teams building regulated digital products that need third-party identity tools connected to production systems, including smart contracts, trading engines, onboarding logic, and enterprise blockchain solutions.

This model is relevant for firms investing in web3 platform development and for operators that need crypto platform compliance solutions embedded in live product workflows rather than isolated compliance screens. The same pattern appears in tokenised assets, prediction markets, AI-led financial products, and cross-chain infrastructure, where the hard part is often less about selecting a verification tool and more about translating regulatory policy into enforceable system behaviour.

For buyers, that leads to a practical conclusion. Vendor evaluation and implementation planning should happen together. If the KYC product supports your policy on paper but your architecture cannot apply those decisions across wallets, accounts, entities, and transactions, the compliance gap remains.

Frequently Asked Questions About KYC Verification

How much do KYC services cost

Pricing varies by provider, workflow complexity, region, and whether you need KYC only or a wider stack that includes KYB, AML screening, and ongoing monitoring. Most buyers should compare commercial models alongside integration effort, manual review burden, and policy flexibility, because the cheapest contract can become the most expensive deployment.

Can KYC be fully automated

Large parts of KYC can be automated, including document checks, liveness, watchlist screening, and risk routing. Full automation is rarely the whole answer in regulated environments, though. High-risk cases, edge documents, complex entity structures, and escalations usually still need human review and policy oversight.

What is the difference between KYC and KYB

KYC verifies an individual customer. KYB verifies a business entity and usually goes further by checking registration status, ownership structure, and ultimate beneficial owners. If your platform serves companies, merchants, funds, or institutional clients, KYB becomes just as important as individual identity verification.

If you’re building a regulated fintech, digital asset product, or AI-enabled platform and need help integrating the right verification stack into production workflows, connect with Blocsys Technologies. The team works with companies designing secure onboarding, policy-aware compliance flows, and scalable infrastructure for blockchain, crypto, and advanced digital finance products.