Most investors assume disruption starts with performance. In fund management, it often starts with plumbing. The strongest evidence around AI-managed investment products doesn’t show a simple race to beat the benchmark. It shows that AI-assisted ETFs have delivered higher Sharpe ratios and lower portfolio volatility than traditional ETFs, and related fund evidence shows lower turnover of 31% for AI funds versus 72% for comparable human-managed funds, which matters because lower turnover reduces transaction costs and operational drag (Alpha Architect’s review of AI funds).

That finding changes the debate. The actual threat to traditional ETFs and wealth management isn’t that AI-powered decentralized funds promise a more exciting story. It’s that they can combine rules-based portfolio logic, on-chain execution, and automated governance into a structure that may be cheaper to run, easier to audit, and more adaptable to modern market infrastructure.

This matters for asset managers, fintech founders, institutional investors, family offices, and digital asset platforms trying to decide what the next operating model for investment products should look like. The question isn’t whether decentralisation alone replaces incumbent products. It’s whether AI plus blockchain can take over the parts of fund management that are repetitive, expensive, opaque, and slow.

Table of Contents

- The End of an Era Why Traditional Wealth Management Is Ripe for Disruption

- What Are AI-Powered Decentralized Funds (DTFs)

- How AI and Smart Contracts Revolutionize Asset Management

- DTF vs ETF vs Traditional Wealth Management A Detailed Comparison

- Navigating the Path to Institutional Adoption

- Real-World Use Cases and The Future of On-Chain Investing

- Build Your Next-Gen Investment Platform with Blocsys

- Frequently Asked Questions about AI-Powered Decentralized Funds

- What are AI-powered decentralized traded funds

- How do DTFs differ from ETFs

- Can AI replace traditional wealth managers

- How do DTFs use blockchain technology

- What are the benefits of AI-powered asset management

- Are decentralized funds suitable for institutional investors

- How can Blocsys build DTF platforms and AI investment solutions

The End of an Era Why Traditional Wealth Management Is Ripe for Disruption

Traditional wealth management still runs on a model built for scarcity. Scarcity of data, scarcity of access, and scarcity of execution speed. Advisers, custodians, transfer agents, administrators, and brokers each play a role, but that layered structure also creates delays, reporting gaps, and cost leakage.

ETFs improved that model by packaging rules-based exposure into a liquid wrapper. But even ETFs remain largely products of centralised operating stacks. Portfolio construction may be systematic, yet servicing, reporting, compliance workflows, and distribution are still fragmented across institutions.

That’s why the fundamental competitive frame isn’t just active versus passive. It’s manual intermediation versus programmable finance. A useful way to think about it is the broader shift described in blockchain vs traditional systems. Once fund logic, ownership records, and transaction history become machine-readable and auditable by design, many back-office functions stop being permanent cost centres.

Why incumbents are vulnerable

Three weaknesses keep showing up in traditional models:

- Operational friction. Human approvals, reconciliations, and off-system reporting slow down execution and oversight.

- Limited transparency. Investors often receive periodic snapshots rather than continuous visibility into how positions, rules, and fees are applied.

- Restricted product adaptability. Custom mandates usually require expensive servicing rather than modular logic that can be updated through code and governance controls.

Traditional wealth management isn’t being challenged because clients dislike advice. It’s being challenged because too much of the operating model still depends on manual coordination.

The result is a market ready for a different format. Not a rejection of pooled investing, but an upgrade to how pooled investing is built, governed, and monitored.

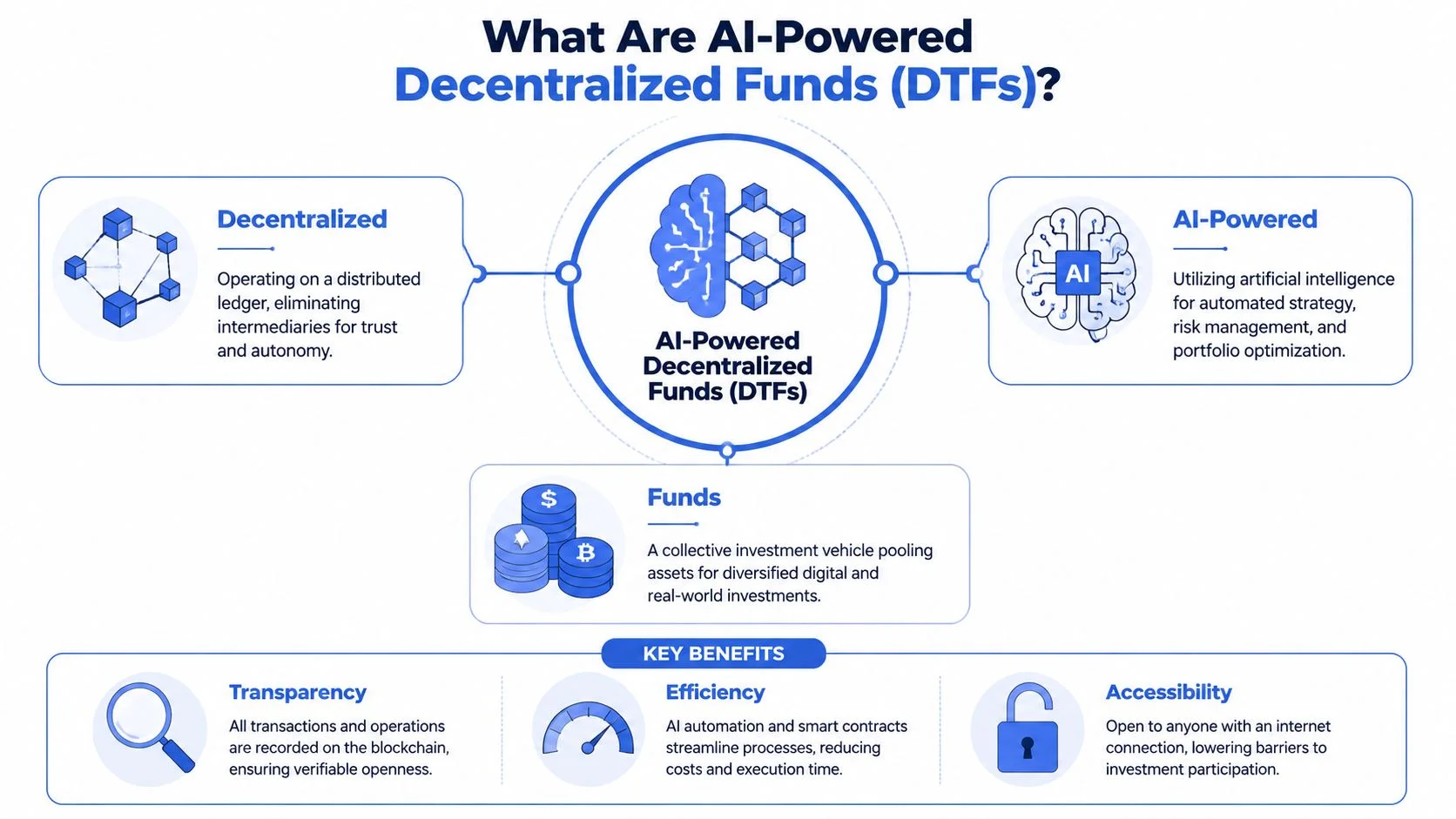

What Are AI-Powered Decentralized Funds (DTFs)

An AI-powered decentralized fund, often called a Decentralized Traded Fund (DTF), is an on-chain investment vehicle that uses smart contracts to manage fund operations and AI models to support portfolio decisions such as allocation, rebalancing, and risk control. In simple terms, it combines the pooled structure of a fund with blockchain-based execution and machine-led decision support.

A working definition for institutional readers

A conventional ETF gives investors exposure to a basket of assets through an exchange-listed structure. A DTF aims to provide a similar basket-based experience, but with a different operating model. The fund logic sits on blockchain infrastructure, ownership can be represented digitally, and rules can be enforced programmatically.

That distinction matters because a DTF isn’t just an ETF on a new database. It’s a fund architecture where asset representation, execution rules, reporting trails, and investor interaction can all be designed as part of the product itself.

What sits inside the model

A practical DTF usually includes four layers.

- Asset layer. The fund may hold native digital assets, tokenized assets, or a mix of both, depending on legal structure and jurisdiction.

- AI layer. Models analyse market signals, portfolio constraints, liquidity conditions, and risk exposures to support allocation decisions.

- Smart contract layer. Code automates subscriptions, rebalancing, fee logic, governance actions, and certain control checks.

- Interface layer. Dashboards, APIs, and reporting tools translate on-chain activity into something portfolio managers, compliance officers, and investors can effectively use.

Why this format is gaining traction

The strongest reason is compatibility with where investment markets are already moving. India is a useful signal. The regulatory foundation for AI-driven and decentralised investment products changed materially when SEBI launched the country’s first spot gold ETF on the National Stock Exchange in 2007. By 2024, Indian ETF assets had expanded to more than ₹7 lakh crore, showing that exchange-traded, rules-based vehicles had become a major part of the domestic investment environment (Journal of Social Science Research analysis).

That doesn’t prove DTF adoption by itself. It does show that investors already understand transparent, pooled, rules-based wrappers. For strategy teams, that means the behavioural hurdle may be lower than expected. The leap isn’t from traditional discretionary advice to code. It’s from one form of rules-based investing to a more programmable one.

Practical rule: If a fund can be expressed clearly as a basket, a mandate, and a set of rebalance conditions, it’s already partway toward a DTF design.

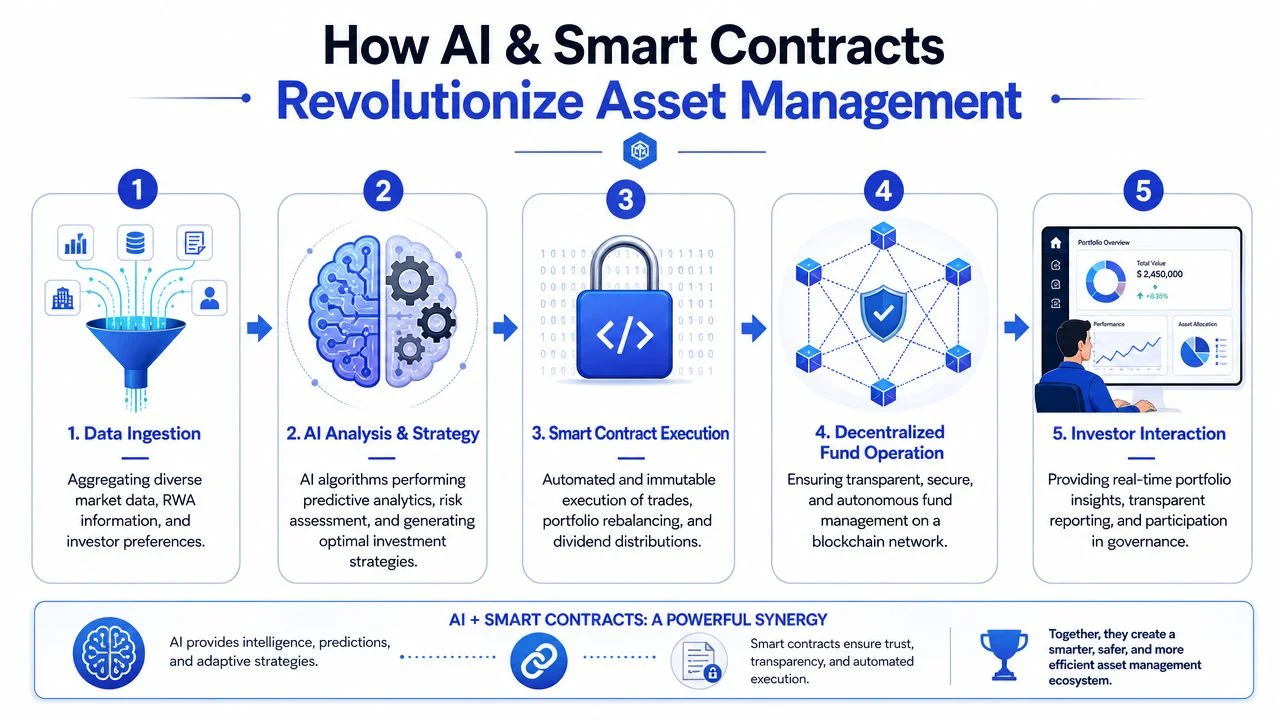

How AI and Smart Contracts Revolutionize Asset Management

DTFs matter because they redesign the operating model of asset management, not just the product wrapper. AI can improve how investment decisions are generated. Smart contracts can improve how those decisions are executed, monitored, and evidenced. For institutional firms, that distinction matters because performance alone does not determine adoption. Control, auditability, and operational resilience do.

AI changes the decision layer

In conventional asset management, research teams, trading desks, risk functions, and operations often work across separate systems with delayed handoffs. AI compresses part of that cycle by processing large sets of market, portfolio, and risk data continuously, then translating them into model-driven recommendations. That can include adjusting weights, identifying correlation breakdowns, flagging volatility regime changes, or screening for mandate breaches before execution.

The practical advantage is not that AI “beats humans” in every context. It is that AI can evaluate more inputs with greater consistency than a portfolio team working through fragmented dashboards and manual review cycles. In institutional settings, that supports a better balance between responsiveness and governance. Models can adapt quickly, while the mandate, risk limits, and approval structure remain clearly defined.

Earlier evidence cited in this article found that AI-driven fund structures were associated with lower turnover and more efficient portfolio management than comparable human-managed approaches. For CIOs and COO teams, the operational implication is as important as the investment implication. Lower turnover can reduce market impact, simplify liquidity planning, and produce cleaner records for internal oversight.

Smart contracts change the execution layer

Execution is where many promising investment models fail institutional scrutiny. A recommendation engine may be sound, but allocators still need confidence that portfolio actions will follow policy, fee logic will be applied correctly, access controls will hold, and records will stand up to compliance review.

Smart contracts address that part of the stack by converting fund rules into deterministic workflows. In a DTF structure, they can automate:

- Rebalancing logic tied to thresholds, calendars, or approved model outputs

- Fee calculation and distribution based on coded terms rather than manual processing

- Permissioning controls for investor onboarding, wallet eligibility, and transfer restrictions

- Operational records that preserve a time-stamped history of actions for audit and reporting

For technical teams evaluating architecture patterns, AI in smart contracts and blockchain automation is the relevant design lens. AI provides adaptive analysis. Smart contracts provide policy enforcement. Institutional-grade DTFs require both, plus the governance layer around them.

Why the combination matters

The strategic shift is architectural. Traditional managers often run research, compliance, administration, and investor servicing as linked but separate functions. DTFs can encode parts of those functions into a shared operating environment where portfolio rules, execution permissions, and reporting records are aligned by design.

That has direct implications for regulation and security. A programmable fund is easier to supervise if mandate logic, access rights, and transaction records are explicit and testable. It is also easier to scale if the underlying infrastructure supports key management, contract audits, oracle integrity, and controlled upgrade paths. Those are the issues that determine whether a DTF remains a niche crypto product or becomes an enterprise-ready fund structure.

The strongest use case is not full automation with humans removed from the process. It is supervised automation, where AI proposes, smart contracts enforce, and human governance retains authority over mandates, exceptions, and model changes. That model fits more naturally with how regulated institutions adopt new infrastructure.

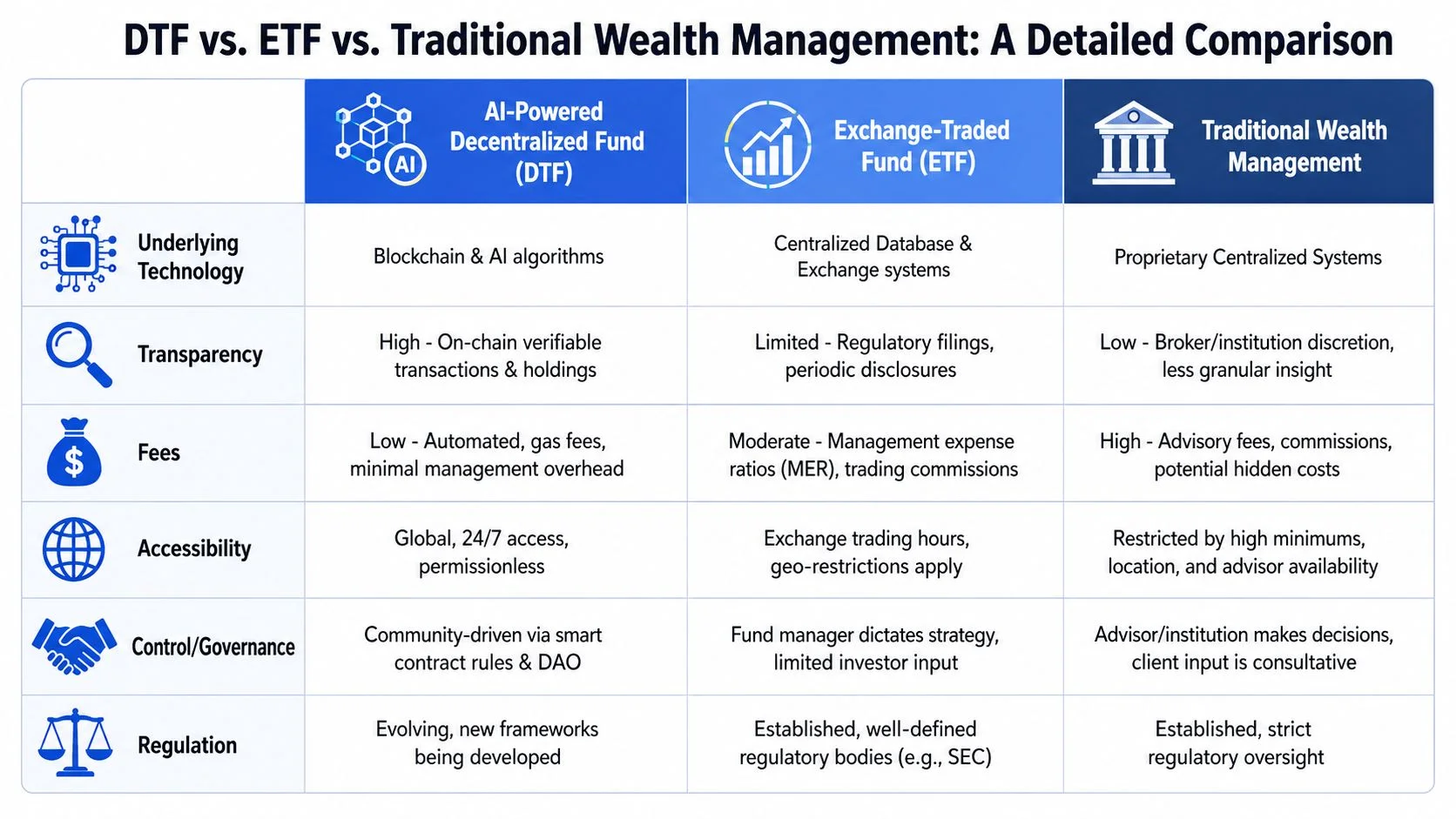

DTF vs ETF vs Traditional Wealth Management A Detailed Comparison

A useful comparison starts with control, not branding. ETFs, DTFs, and traditional wealth management all pool capital or direct capital. What differs is how they handle decision-making, transparency, servicing, and investor access.

Where each model fits

ETFs remain efficient where investors want standardised exposure, familiar regulation, and exchange-based liquidity. Traditional wealth management remains relevant where clients need bespoke planning, tax structuring, and relationship-led service. DTFs fit where investors and operators value programmability, automated controls, and closer-to-real-time transparency.

For institutions evaluating DeFi ETFs and custodian product models, the issue is less about replacing one product with another overnight. It’s about identifying which parts of the stack can migrate first. In many cases, reporting, treasury logic, rebalancing, and tokenized exposure can move before full fund redesign.

Comparison table

| Feature | AI-Powered DTF | Traditional ETF | Traditional Wealth Management |

|---|---|---|---|

| Core operating model | On-chain, rule-based, automated through smart contracts and AI-supported workflows | Exchange-traded pooled vehicle managed through centralised market infrastructure | Human-led advisory and portfolio servicing through institutional platforms |

| Portfolio decisions | Model-assisted and programmable within defined mandates | Usually index-tracking or manager-defined methodology | Adviser, committee, or portfolio manager discretion |

| Execution | Can be automated directly in protocol logic | Executed through market intermediaries and fund operations processes | Routed through custodians, brokers, and operations teams |

| Transparency | Potentially high, with auditable on-chain activity and programmable reporting | Periodic disclosures and standard fund reporting | Dependent on adviser reporting, client portals, and back-office systems |

| Customisation | High, because strategies can be structured as code and governance rules | Moderate, but generally limited to the published mandate | High for large accounts, but usually expensive to deliver |

| Availability | Can support continuous digital interaction, subject to legal and technical design | Exchange hours and market structure constraints | Service availability depends on institution and adviser model |

| Governance | Can include embedded voting, policy rules, or automated controls | Governed by fund sponsor and regulatory framework | Governed by adviser agreements and internal committees |

| Operational dependency | Lower reliance on manual middle and back-office coordination | Moderate reliance on administrators, exchanges, and custodians | High reliance on relationship managers and institutional workflows |

| Best use case | Programmable investment products, tokenized funds, on-chain strategies | Broad market access through familiar wrappers | Bespoke planning and high-touch advisory relationships |

A few implications stand out.

- DTFs compress administration into product design. Instead of building oversight around the fund after launch, teams can encode parts of oversight into the fund from day one.

- ETFs still win on familiarity. That matters with boards, pension committees, and conservative distribution channels.

- Traditional wealth management still owns trust-heavy relationships. Family governance, succession planning, and complex suitability conversations aren’t disappearing because a model can rebalance a basket.

If you’re choosing between these models, the question isn’t which one is superior in abstract terms. The question is which operating burden you want to keep paying for.

That’s why DTFs are more likely to replace selected layers of ETF administration and discretionary portfolio management before they replace every incumbent structure.

Navigating the Path to Institutional Adoption

Institutional adoption won’t be blocked by lack of interest. It will be gated by whether firms can satisfy compliance, custody, governance, and infrastructure requirements without breaking the economic case for the product.

Regulation is the real gatekeeper

Most commentary on AI-powered decentralized funds spends too much time on automation and not enough on admissibility. In regulated markets, that’s backwards. If a DTF can’t support KYC, AML controls, suitability logic, disclosure standards, and auditable governance, it won’t matter how elegant the code is.

That’s why the Indian market offers a useful lesson. The rapid growth of the ETF market to over ₹7 lakh crore by 2024 shows broad investor acceptance of transparent, rules-based investment vehicles. At the same time, a major hurdle for DTFs is the complexity of KYC, AML, and custody rules enforced by bodies such as SEBI and the RBI, a nuance often missed in technology-first discussions (VanEck’s discussion of AI and wealth management).

The same lesson applies globally. In the USA, UK, EU, UAE, Singapore, Luxembourg, and Switzerland, the winning DTF model will be the one that fits existing supervisory expectations rather than pretending they don’t matter.

Security and scale are engineering questions

Once regulation is taken seriously, the next challenge is operational resilience. Institutional-grade DTF infrastructure needs more than a token contract and a dashboard. It needs clear permissioning, secure custody design, tested smart contracts, event monitoring, policy enforcement, and service recovery planning.

A sensible institutional checklist includes:

- Code assurance. Smart contracts need formal review, staged deployment, and well-defined upgrade controls.

- Data governance. If AI models influence allocations, firms need versioning, approval workflows, and evidence for how model outputs were used.

- Custody architecture. Asset control has to match the legal structure of the fund and the obligations of the manager.

- Scalability planning. High-volume subscriptions, redemptions, and rebalancing events require infrastructure that won’t fail when activity clusters.

For boards following institutional blockchain adoption trends and implementation challenges, that’s the practical inflection point. DTFs become credible when firms stop treating them as experimental DeFi wrappers and start treating them as regulated digital products with explicit control frameworks.

Institutions won’t adopt DTFs because decentralisation sounds modern. They’ll adopt them when the control environment is stronger, cheaper, or faster than the current one.

Real-World Use Cases and The Future of On-Chain Investing

The strongest use cases for DTFs are the ones where programmability solves an obvious operational problem. Not every fund needs to be on-chain. The ones that do usually involve frequent rebalancing, transparent rule sets, multi-asset coordination, or tokenized underlying exposure.

Where DTFs are most credible today

One credible application is a digital asset allocation fund where model-driven rules shift exposure between liquid tokens based on volatility, liquidity, and predefined risk parameters. Another is a tokenized real-world asset basket, where a fund manages exposure to assets such as precious metals or other tokenized claims through programmed allocation logic rather than manual dealing processes.

A third use case sits between ETFs and structured products: thematic on-chain funds. These can track sectors such as decentralised AI infrastructure, blockchain middleware, or tokenized collateral networks. The attraction isn’t novelty. It’s that the strategy can be inspected, updated through governance, and monitored with clearer operational telemetry than many legacy wrappers provide.

Teams exploring tokenized exposure often start with adjacent building blocks such as real-world asset tokenization and how it works on blockchain. That’s usually the bridge from a conventional pooled product to a more programmable one.

What the next 12 to 24 months are likely to bring

The near-term future is less about fully autonomous hedge funds and more about modular adoption. Three developments look especially plausible.

- Model-guided mandate overlays. Existing fund products may use AI to support dynamic risk bands, allocation triggers, or treasury policies before moving fully on-chain.

- Personalised pooled products. Managers may offer strategy variants that adjust exposures within approved parameters for different investor cohorts.

- Embedded compliance logic. More products will treat onboarding, disclosures, and transfer restrictions as part of the infrastructure, not an afterthought.

The surprising conclusion is that DTFs may first replace parts of the middle office, not the front office. Firms are likely to adopt them because they improve control, monitoring, and operational consistency. Portfolio innovation follows after that.

Build Your Next-Gen Investment Platform with Blocsys

The hard part of launching an AI-powered decentralized fund isn’t writing a strategy memo. It’s turning that strategy into a product that can survive legal review, technical scrutiny, and institutional due diligence.

That requires several capabilities at once: smart contract architecture, tokenization design, wallet and custody flows, reporting pipelines, AI-assisted decision systems, and compliance-aware product logic. Teams also need to decide which functions should stay off-chain, which should be codified, and which should be governed through configurable policies.

One practical route is to work with engineering partners that already build blockchain-based financial infrastructure. Blocsys Technologies develops production-ready digital asset platforms, tokenization systems, and AI-powered financial applications for fintechs, exchanges, and institutional product teams. If you’re modelling delivery effort across modules such as custody, trading, and compliance tooling, the software development cost estimator from Blocsys is a useful scoping reference.

For product teams expanding AI capability beyond fund logic, this guide to AI development for full-stack projects is also useful because it frames how application-layer AI should connect with production systems rather than sit beside them.

The firms that move first won’t win because they used more buzzwords. They’ll win because they designed an operating model that regulators, auditors, and investors can trust.

Frequently Asked Questions about AI-Powered Decentralized Funds

What are AI-powered decentralized traded funds

AI-powered decentralized traded funds combine three layers in one investment product: an investment model, programmable fund operations, and an on-chain record of ownership and activity. The important distinction is operational. A credible DTF is not just a tokenized fund with an AI label. It needs defined model governance, contract controls, exception handling, and auditability that can withstand legal, risk, and compliance review.

How do DTFs differ from ETFs

The biggest difference is not distribution. It is control architecture. ETFs rely on a mature chain of intermediaries to handle creation and redemption, pricing oversight, custody, and investor protections. DTFs can shift part of that control into code, which changes where operational risk sits.

For institutions, that creates a different diligence process. The key questions move toward oracle design, smart contract upgrade rights, key management, valuation methodology for less liquid assets, and whether the product can support compliance obligations such as transfer restrictions or investor whitelisting.

Can AI replace traditional wealth managers

AI can automate parts of portfolio construction, monitoring, tax-aware rebalancing, and client segmentation. It does not absorb fiduciary accountability. In regulated settings, someone still owns mandate design, suitability, model validation, escalation decisions, and client communication.

A common misconception is that better prediction alone makes an investment system institution-ready. It does not. Firms adopting AI in asset management usually get more value from disciplined process control than from headline forecasting gains, especially where governance committees, model risk teams, and regulators expect documented oversight.

How do DTFs use blockchain technology

Blockchain is useful in DTFs because it can provide a shared operational record across managers, administrators, custodians, and auditors. That matters most in processes that usually break across systems, such as entitlement tracking, corporate actions processing, fee accrual logic, and restricted transfer enforcement.

The practical design choice is what stays on-chain and what does not. Many institutional-grade products keep sensitive analytics, parts of trade decisioning, and certain investor data off-chain, while using the chain for state changes, ownership records, control logic, and proofs of process integrity.

What are the benefits of AI-powered asset management

The strongest benefit is consistency at scale. AI systems can screen large opportunity sets, apply the same mandate logic across accounts, and flag drift or anomalies faster than manual review cycles usually allow.

There is also a product design benefit. Managers can encode more precise investment rules, fee logic, and risk triggers, then test how those rules behave under different market conditions before launch. That makes new fund structures easier to evaluate from an operating-model perspective, not just an investment thesis perspective.

Are decentralized funds suitable for institutional investors

They can be, if the structure meets institutional requirements rather than crypto-native expectations. That usually means clear legal wrappers, audited contracts, controlled governance, qualified custody or an equivalent control framework, incident response procedures, and reporting that fits existing compliance and finance workflows.

Adoption often starts in narrower segments first. Treasury products, private market feeder structures, or strategy sleeves inside a broader digital asset platform are generally easier to approve than fully open retail-style funds. Institutions rarely reject the concept because it is on-chain. They reject products that create unresolved legal, control, or operational gaps.

How can Blocsys build DTF platforms and AI investment solutions

Blocsys can support firms that need the underlying system design for a DTF or adjacent on-chain investment product. That includes tokenization architecture, smart contract implementation, wallet and custody flows, compliance-aware transfer logic, and integration points between AI models and production fund infrastructure.

If your firm is assessing AI-powered decentralized funds, tokenized investment products, or on-chain asset management infrastructure, Blocsys Technologies can help you translate strategy into buildable architecture. Connect with the team to evaluate product design, compliance-aware workflows, and engineering options for your next investment platform.