Institutional interest in tokenised assets is no longer a niche experiment. Independent market analysis says the global real-world asset market reached about $24 billion in 2025, up 308% over three years, with projections of up to $30 trillion by 2034 according to Katten’s analysis of the tokenization market. For banks, asset managers, and market infrastructure providers, that changes the conversation. The question isn’t whether tokenisation matters. It’s which stack can support it without breaking legal workflows, control frameworks, and operational discipline.

That’s where DAML becomes relevant. Financial institutions don’t need another token standard in isolation. They need a way to encode ownership rules, transfer restrictions, lifecycle events, and settlement logic so that the digital representation of an asset stays aligned with the legal and operational reality behind it. This article is written for innovation committees, digital asset leads, compliance teams, and enterprise architects evaluating that decision.

The practical outcome is straightforward. You’ll see where DAML fits in the RWA stack, what it solves better than legacy workflows or generic public-chain contracts, where interoperability remains the hard problem, and how implementation should be framed if the objective is regulated, production-grade tokenisation rather than a proof of concept.

Table of Contents

- The Trillion-Dollar Opportunity in Real-World Asset Tokenization

- What is DAML and Why Is It Built for Institutional Finance

- DAML vs Traditional Systems and Public Blockchains

- The Complete RWA Tokenization Workflow with DAML

- Solving Interoperability and Privacy with the Canton Network

- How Blocsys Builds Enterprise-Grade DAML Tokenization Platforms

- Frequently Asked Questions on DAML for RWA Tokenization

The Trillion-Dollar Opportunity in Real-World Asset Tokenization

Why the market signal matters now

Independent market analysis estimated the global RWA tokenization market at about $24 billion in 2025, up 308% over three years, while the same analysis cited rwa.xyz figures of $31.96 billion in distributed asset value and $342.20 billion in represented asset value. As noted earlier, Katten’s legal and market review also points to long-range projections measured in the trillions.

For a bank, those figures are less interesting as headline growth than as an infrastructure signal. If tokenised instruments become a meaningful part of issuance, servicing, collateral management, or investor distribution, the economic question shifts from “can we mint an asset” to “can we operate it under policy, at scale, with low control failure rates.”

That is the true opportunity.

Returns do not come from token creation alone. They come from shortening post-trade processes, reducing reconciliation work, tightening transfer controls, improving collateral mobility, and lowering the cost of proving compliance across the asset lifecycle. Those benefits depend on governance and workflow design, not on the existence of a token standard.

A useful way to evaluate the market is to separate three layers of value:

- Digital representation: creating the token or record that maps to the underlying asset.

- Operational control: enforcing entitlements, approvals, restrictions, lifecycle events, and exception handling.

- Institutional deployment: integrating those controls with legal agreements, custody models, existing systems, and supervisory expectations.

Many tokenisation programmes stall at the second layer. The reason is straightforward. Issuing a digital instrument is technically simple relative to running a regulated instrument across multiple parties who do not share the same systems, incentives, or permissions.

Why DAML matters more than a token wrapper

This is why firms assessing real-world asset tokenization platforms for regulated institutions should look beyond issuance mechanics. The hard problem is not representing an asset on a ledger. The hard problem is making each state change valid, observable to the right parties, and enforceable under operating rules that auditors, risk teams, and regulators can examine.

DAML is relevant here because it models the behaviour of the asset, not just its digital form. That means eligibility checks, approval chains, settlement conditions, corporate actions, and redemption logic can be expressed as part of the application itself rather than patched together across middleware, manual controls, and bilateral procedures.

Practical test: If the platform cannot define who may act, under what conditions they may act, what approvals are required, and what record of that action must persist, it does not solve the institutional RWA problem.

The strategic implication is easy to underestimate. In financial institutions, tokenisation succeeds when governance becomes programmable and portable across workflows, not when an asset is wrapped and placed on another ledger. DAML addresses that operating model directly, which is why it deserves attention from committees evaluating risk, compliance, and long-term return on infrastructure investment.

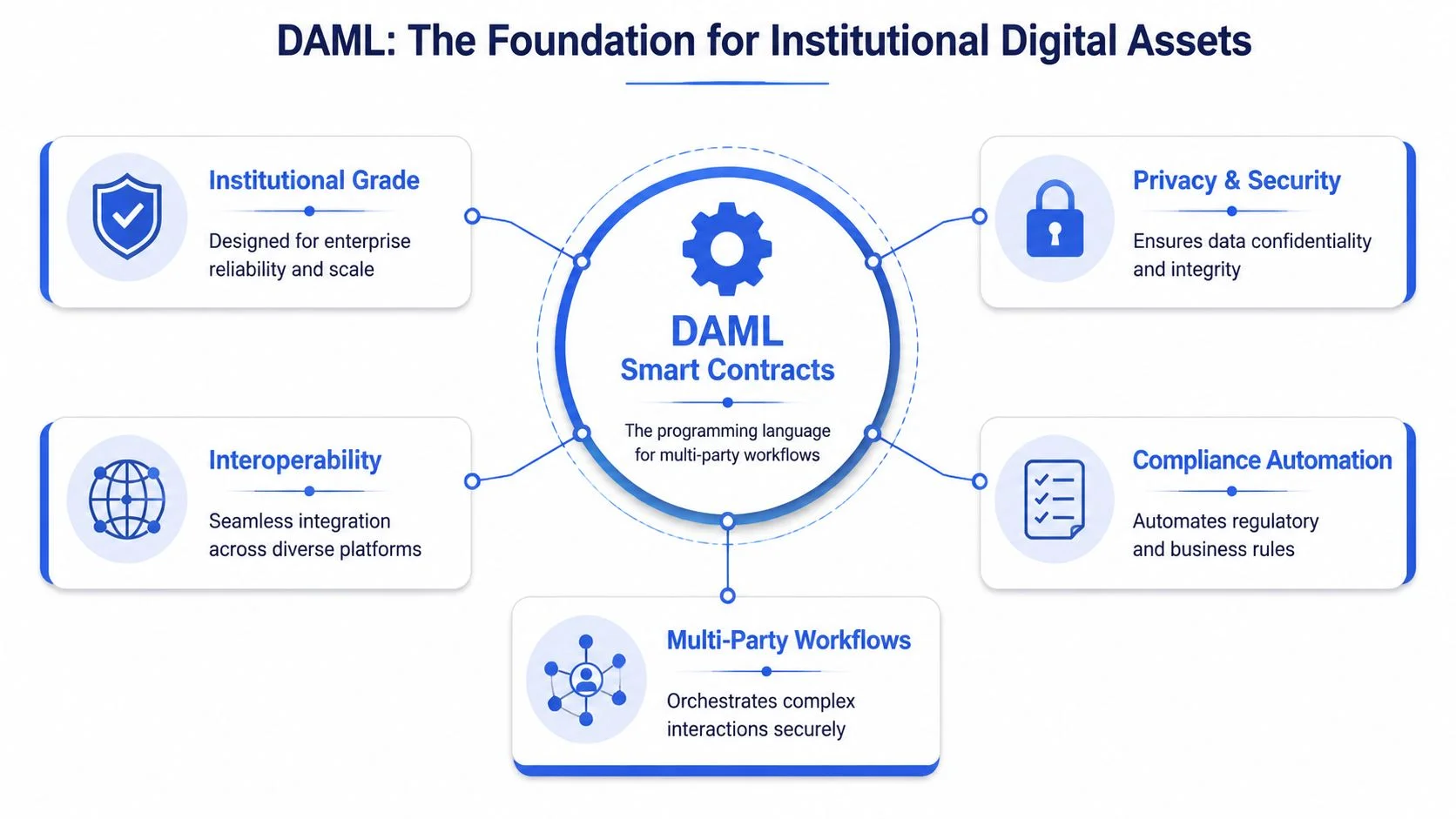

What is DAML and Why Is It Built for Institutional Finance

DAML is a workflow language, not just a contract language

DAML is best understood as a language for modelling multi-party business processes. That sounds abstract until you place it in a capital-markets context. A tokenised bond, fund unit, treasury instrument, or private credit position isn’t controlled by one actor. It touches the issuer, custodian, transfer agent, investor, operations team, and often a compliance function as well.

Digital Asset’s description is unusually close to the practical implementation concern. It describes DAML as a platform for building and running advanced multi-party applications that “extracts and simplifies business processes” in its overview of asset tokenisation with DAML. That wording matters because institutions don’t usually fail at tokenisation due to lack of ledger technology. They fail when the business process remains fragmented across teams and systems.

A useful mental model is this: DAML turns a legal and operational agreement into a controlled state machine shared by the right parties, with permissions and transitions defined in the contract logic.

For readers evaluating the design from first principles, this is also a helpful background on what DAML means as an enterprise smart contract framework.

What that means for a regulated asset

The strongest technical point is that DAML models an asset as a bundle of enforceable rights and obligations across all parties, which is exactly how institutions already think about financial instruments in practice. A security is never just an entry in a ledger. It is a set of claims, permissions, duties, and event-driven processes.

That changes how engineers and business owners should define scope.

- Issuance logic isn’t only minting. It includes who is authorised to create the position, under what terms, with what investor constraints.

- Transfer logic isn’t only movement. It includes eligibility, consent, restrictions, and record updates across participants.

- Lifecycle logic isn’t only automation. It includes corporate actions, payment events, notices, redemptions, and exceptions.

DAML is most useful where firms need the asset and its workflow to remain coupled. Once those drift apart, reconciliation cost returns.

For a bank, that coupling reduces a familiar problem. Teams no longer have to maintain separate versions of the truth across middle-office systems, transfer records, and bilateral communication chains. DAML doesn’t remove legal process, but it can make the workflow itself computationally enforceable.

That’s why DAML fits institutional finance better than the usual “smart contracts automate everything” narrative. Its real contribution is discipline. It forces the asset model to reflect the actual rights and obligations that regulated participants must honour.

DAML vs Traditional Systems and Public Blockchains

Where legacy infrastructure breaks down

The business case becomes sharper when compared with current operating models. Traditional securities settlement still commonly runs on T+2 cycles, while tokenised assets can settle in seconds, reducing intermediary handoffs and back-office reconciliation according to Propeller’s analysis of tokenized asset operations.

That time gap isn’t just a speed issue. It affects collateral efficiency, liquidity usage, exception handling, and operational staffing. Delayed finality keeps capital tied up and creates room for mismatched records between participants.

Three pain points usually sit underneath the T+2 problem:

- Fragmented records: each participant keeps its own system of record and reconciles after the fact.

- Manual controls: transfer restrictions and approvals often live in procedures rather than executable logic.

- Lifecycle friction: servicing events require coordination across multiple systems and teams.

Why public chains create a different risk profile

Public blockchains solve programmability, but they don’t automatically solve regulated workflow design. For many institutions, the challenge isn’t whether a token standard exists. It’s whether privacy, role-based control, and deterministic business logic can be enforced without exposing commercially sensitive information or forcing a one-size-fits-all operating model.

DAML sits in the middle. It brings programmability, but its orientation is institutional workflow rather than retail token issuance.

| Feature | Traditional Systems | Public Blockchains (e.g., Solidity) | DAML |

|---|---|---|---|

| Settlement speed | Commonly T+2 | Can support rapid settlement | Supports policy-driven workflows for rapid settlement scenarios |

| Privacy model | Usually controlled within enterprise systems | Often difficult to align with institutional confidentiality requirements | Designed for regulated multi-party workflows with controlled visibility |

| Compliance handling | Often externalised into manual checks and procedures | Often requires custom logic around generic token standards | Encodes institutional rules directly into deterministic workflows |

| Reconciliation burden | High across participants and systems | Can reduce some ledger duplication, but workflow fragmentation may remain | Reduces reconciliation by aligning parties to shared contract state |

| Lifecycle management | Distributed across separate systems | Often built as application logic around token contracts | Built around atomic, policy-driven lifecycle transitions |

| Institutional fit | Familiar but operationally slow | Programmable but not naturally shaped for regulated finance | Purpose-built for multi-party financial agreements |

The wrong comparison is “blockchain versus no blockchain”. The right comparison is “which execution model lowers operational risk without weakening control”.

If you’re evaluating language and platform choices, this is also the key issue behind DAML vs Solidity in enterprise settings. Solidity is effective for public-chain applications. DAML is better suited when the asset is inseparable from legal roles, permissions, and coordinated institutional processes.

The Complete RWA Tokenization Workflow with DAML

A practical lifecycle using a tokenised bond

For a bank or market infrastructure provider, tokenisation succeeds only if the digital asset behaves like the underlying instrument under real operating conditions. A tokenised corporate bond is a useful example because it carries clear legal terms, recurring servicing events, transfer restrictions, and a defined maturity profile. The delivery challenge is to represent those obligations in software without creating new manual controls around the ledger.

DAML addresses that problem by modelling the bond as a governed agreement between identified parties, not as a generic on-chain unit. That distinction matters in production. Institutions need issuance controls, investor eligibility checks, approval paths, payment handling, and exception management to operate as one coherent workflow.

1. Asset identification and structuring

The institution first defines the legal wrapper, distribution model, investor restrictions, settlement path, servicing obligations, and custody model. This phase usually determines whether the programme will scale. If those requirements remain in policy documents while the ledger tracks only ownership, the operating model still depends on manual interpretation and post-trade repair.

2. DAML contract definition

The bond’s rights and obligations are then encoded into DAML contracts. That includes issue size, party roles, transfer constraints, corporate action logic, payment events, and redemption conditions. The result is not a simple token record. It is an executable representation of how the instrument is allowed to move through its lifecycle.

3. Issuance and allocation

Once legal, compliance, and operational approvals are complete, the instrument can be issued to eligible counterparties. DAML enforces the transition from pre-issue setup to live holdings through explicit workflow choices and party permissions. That reduces dependence on side agreements, email instructions, or manual reconciliations at the point of issuance.

What the operating model looks like in production

Issuance is usually the easiest milestone to demonstrate and the least important one to optimise. Financial institutions realise value after issuance, where most operational cost and control failures occur. Teams evaluating RWA tokenization services built for enterprise assets should focus on whether the platform can carry the asset through servicing, transfer, and final redemption under policy.

A DAML-based production lifecycle typically includes four categories of events:

Coupon and payment processing

Scheduled events can initiate the correct state transitions, notify the relevant parties, and preserve an auditable record of entitlement and payment status.Secondary transfers with embedded controls

Transfer requests can be checked against role permissions, holding restrictions, jurisdiction rules, and approval requirements before ownership changes.Role-specific operations

Issuers, investors, custodians, paying agents, and administrators act within defined rights. That is closer to how regulated institutions operate than a wallet-centric model.Maturity, redemption, and closeout

The final lifecycle event can retire the instrument in line with contractual terms while maintaining a consistent history of positions, approvals, and obligations.

The critical question is whether the delivery team can model the full asset lifecycle without splitting governance across separate systems. If post-issuance events still rely on spreadsheets, middleware patches, and email approvals, the institution has digitised a record, not the operating process.

A useful way to frame DAML in this workflow is as two connected control layers:

| Workflow layer | What DAML handles |

|---|---|

| Contract state | Ownership, rights, obligations, approvals |

| Operational events | Transfers, servicing, redemptions, role-based actions |

That design has direct ROI implications. Middle and back office teams usually see the first gains through fewer exceptions, lower reconciliation effort, clearer audit trails, and tighter policy enforcement. Front-office liquidity narratives may attract attention, but governance and workflow automation are what determine whether an institutional tokenisation programme can pass risk, compliance, and operations review.

For institutions assessing deployment models, Blocsys also outlines Canton Network use cases for finance in Europe. For ecosystem talent tracking, teams can also explore DevRel opportunities.

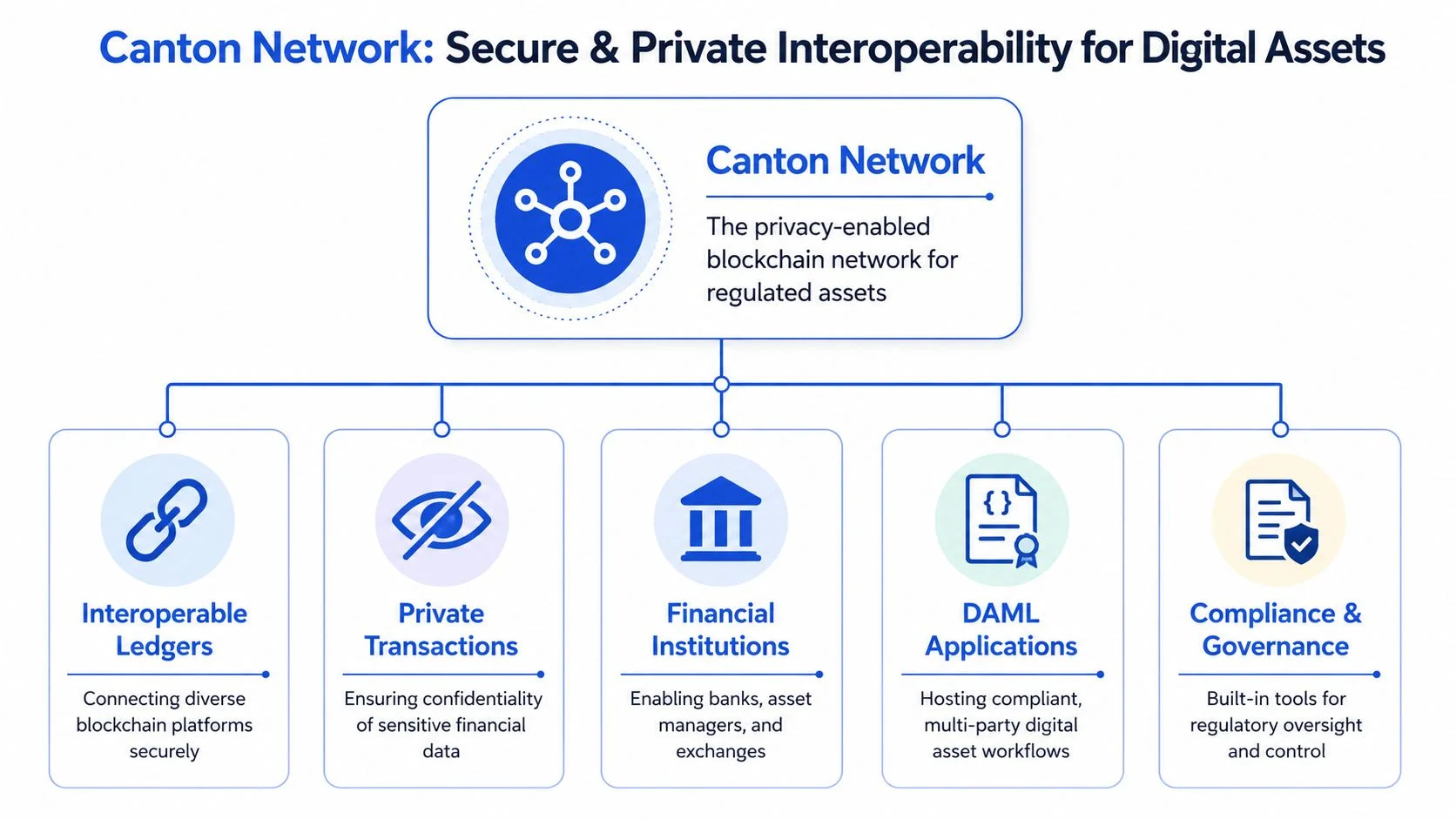

Solving Interoperability and Privacy with the Canton Network

Tokenisation fails if it creates new silos

A major institutional concern is easy to overlook when tokenisation is discussed mainly in terms of liquidity. A tokenised asset isn’t especially useful if it remains trapped inside one venue, one custodian environment, or one permissioning scheme. The harder question is whether tokenisation reduces reconciliation and settlement friction across platforms, not only within a single application.

That concern has been stated clearly in Fintech Weekly’s institutional analysis of tokenisation fragmentation. The critique is that fragmentation is a first-order risk. Assets tokenised on one platform may not be usable on another without common approaches to identity, settlement, and transfer rules. The same analysis argues that DAML provides the programmable rights and obligations layer, but Canton is needed to address cross-platform liquidity and settlement without creating new silos.

The failure mode for institutional tokenisation isn’t usually technical impossibility; it’s local optimisation. One platform works well on its own, but the market becomes harder to coordinate overall.

Privacy without interoperability creates islands. Interoperability without privacy creates compliance problems.

Why Canton complements DAML

DAML and Canton solve different parts of the architecture. DAML handles the application and contract logic. Canton addresses the problem of connecting independent systems in a way that preserves confidentiality while allowing coordinated transactions.

For a financial institution, that produces a more credible operating model:

- Selective disclosure: participants don’t need to expose every transaction to every other participant.

- Cross-application coordination: assets and workflows can interact without collapsing into a single shared database model.

- Institutional governance: firms can keep control boundaries while still participating in a networked asset environment.

That’s why many architecture committees now treat interoperability as a prerequisite rather than an enhancement. The question isn’t whether a token can move. It’s whether the surrounding systems can recognise, trust, and process that movement without duplicative reconciliation.

Teams tracking talent and ecosystem maturity may also want to explore DevRel opportunities around Canton-related infrastructure, because developer enablement is becoming part of the broader institutional adoption picture.

For organisations evaluating design patterns in regulated markets, this is the practical context behind enterprise blockchain use cases for finance on Canton-style infrastructure. DAML gives the institution a precise workflow language. Canton makes it more realistic to connect those workflows beyond one isolated implementation.

How Blocsys Builds Enterprise-Grade DAML Tokenization Platforms

What an implementation partner should actually deliver

Most institutions don’t need help understanding that tokenisation is strategically relevant. They need help translating policy, legal structure, and operating controls into a production system. That means the implementation partner must think like both a systems architect and a controls engineer.

A credible DAML delivery scope usually includes:

Asset and workflow modelling

The project should begin with ownership structure, participant roles, transfer constraints, lifecycle events, and exception paths.Contract implementation

DAML contracts need to reflect operational truth, not a simplified demo path.Integration design

The platform has to connect to custody, reporting, compliance, and internal operational systems.Governance controls

Entitlements, approvals, auditability, and change management must be designed from the start.

One practical route for firms building that capability is an enterprise blockchain tokenization platform approach. In that context, Blocsys Technologies is one implementation option for teams that need custom tokenisation infrastructure, DAML-oriented workflow design, and integration support around enterprise digital asset systems.

The key selection criterion isn’t whether a vendor can mint tokens. Plenty can. The critical question is whether the delivery team can model the full asset lifecycle with enough precision that compliance, operations, and product teams all recognise the system as usable.

For banks and asset managers, that usually means starting narrowly. Pick one asset class, one workflow family, and one control perimeter. Prove that issuance, transfer, and servicing can run against shared logic. Then expand from there.

Frequently Asked Questions on DAML for RWA Tokenization

What is DAML language

DAML is a smart contract language built for multi-party business workflows in finance. It is designed to model assets as enforceable rights and obligations shared across the relevant participants rather than as standalone tokens.

How does DAML support RWA tokenization

DAML supports RWA tokenization by encoding issuance rules, transfer restrictions, participant permissions, lifecycle events, and settlement logic directly in the contract workflow. That helps keep the digital asset aligned with the legal and operational structure behind it.

Why do financial institutions use DAML instead of generic smart contracts

Institutions use DAML when they need more than token programmability. They need deterministic workflows, role-aware permissions, and a contract model that reflects issuers, custodians, transfer agents, and investors operating under regulated conditions.

How does DAML relate to the Canton Network

DAML handles the business logic and workflow layer. Canton addresses privacy-preserving interoperability across systems and applications. Together, they address a common institutional requirement: coordinated asset operations without exposing sensitive data broadly.

What assets can be tokenised using DAML

Digital Asset positions DAML as asset-agnostic and purpose-built for finance, used to tokenize regulated assets, liabilities, and agreements including public and private securities, digital cash, treasuries, money market funds, commodities, carbon, and mortgages in its tokenization use case overview. The same source notes the digital rupee pilot in India reached 1 million users by 2023, which shows that regulated digital money infrastructure is already becoming operationally relevant in some markets.

How can an institution get started

Start with one asset class where workflow friction is already visible. Define the legal structure, participant roles, compliance constraints, servicing events, and integration requirements before choosing the ledger architecture. That sequence usually produces a better result than starting from the token standard.

Banks, asset managers, and digital asset teams that want to move from tokenisation strategy to implementation can connect with Blocsys Technologies to discuss DAML-based workflow design, regulated asset platforms, and enterprise blockchain delivery options designed for real operating constraints.