A bank innovation committee usually sees the same pattern first in operations, not strategy. Onboarding queues get longer. Exception handling grows faster than automation. Fraud teams spend more time proving whether a document was altered than deciding what to do next.

That’s why the conversation around blockchain customer document verification has changed. It’s no longer about abstract immutability. It’s about whether banks can create a verification layer that is reusable, auditable, privacy-aware, and compatible with real compliance workflows. For banks, fintechs, and digital identity teams evaluating secure banking document authentication, the practical question isn’t “should we put documents on a blockchain?” It’s “what part of the verification process benefits from a shared tamper-evident record, and what still needs traditional controls?”

This guide is written for decision-makers who need a grounded view of how banks use blockchain for secure customer document verification, what works in production, and where the risks still sit.

Table of Contents

- The Rising Tide of Document Fraud and Verification Inefficiency

- How Blockchain Creates a Tamper-Proof Verification Layer

- A Strategic Blueprint for Implementing Blockchain Verification

- Use Cases, Critical Risks, and the Future of Decentralized Identity

- Build Your Enterprise-Grade Verification Platform with Blocsys

- Frequently Asked Questions about Blockchain Banking Verification

- How does blockchain improve banking document verification

- What is blockchain KYC verification

- How do banks use blockchain for customer authentication

- Does blockchain stop document fraud by itself

- What are tamper-proof banking verification systems

- Why are banks adopting blockchain verification

- How can Blocsys help build blockchain banking verification systems

The Rising Tide of Document Fraud and Verification Inefficiency

A typical compliance queue now contains more than expired passports and unclear utility bills. Teams deal with edited PDFs, mismatched metadata, recycled corporate records, and applicants who may have already completed KYC at another institution but still need to repeat the entire process. That repetition creates cost, delay, and risk.

Why manual verification breaks under volume

Traditional customer verification systems usually depend on a central repository, email attachments, scanned copies, and internal review notes spread across disconnected tools. Even when the workflow is digital, the logic is often still manual. One analyst checks the document, another confirms the address, and a third reviews exception flags.

That design has two weaknesses. First, it doesn’t produce a reusable proof that another approved institution can trust. Second, it leaves too much operational value trapped inside one bank’s internal process. The result is duplicated onboarding and inconsistent evidence trails.

A similar issue appears outside banking. In property and rental workflows, identity and background checks also suffer when verification data is fragmented across systems. A practical example is this UK tenant screening background check, which shows how trust decisions become slower and more expensive when every check starts from scratch.

Practical rule: If the same identity document must be checked repeatedly by different institutions, the problem isn’t only fraud detection. It’s the lack of portable trust.

Banks also face a harder environment than most sectors. The fraud threat is active, the compliance threshold is high, and the customer expects instant onboarding. Those pressures don’t sit well with branch-era verification models.

Why the market is moving anyway

Adoption has advanced because banks are no longer treating blockchain as a lab-only technology. In financial services, banking accounts for roughly 29–30% of blockchain usage across industry verticals, and traditional banks increased blockchain adoption by 47.3% while fintech firms reached 68.9% in a recent study, according to this financial services blockchain statistics report.

That matters because document verification is one of the few banking workflows where blockchain’s strengths are operationally clear. A tamper-evident record, shared verification logic, and controlled reuse of prior checks can improve both customer experience and internal assurance.

For committees assessing whether this is a real enterprise shift, it helps to look at how firms are thinking about broader trust infrastructure, not only crypto-native systems. This is also why many banks are studying tamper-proof verification platforms as part of a wider digital identity and compliance modernisation plan.

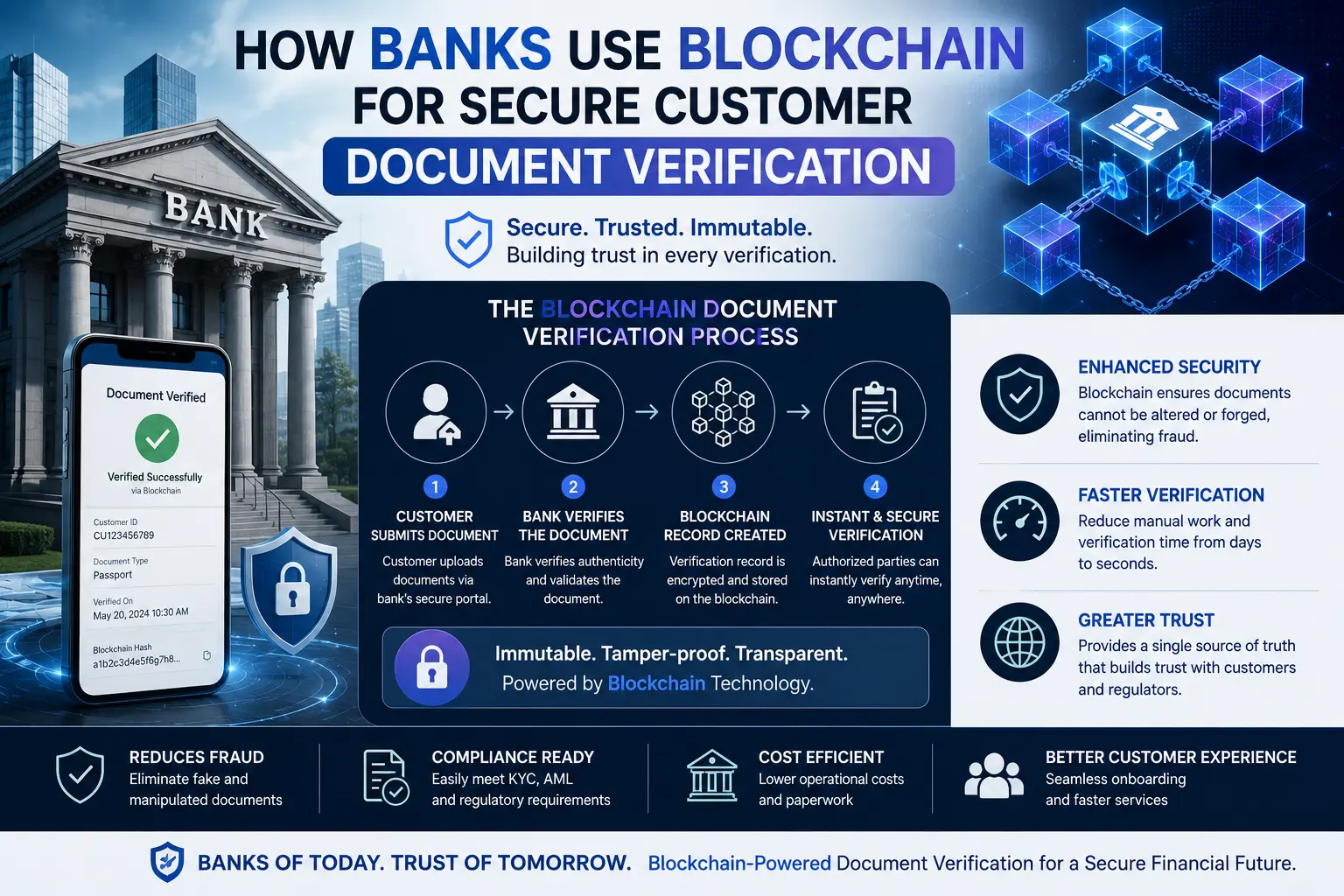

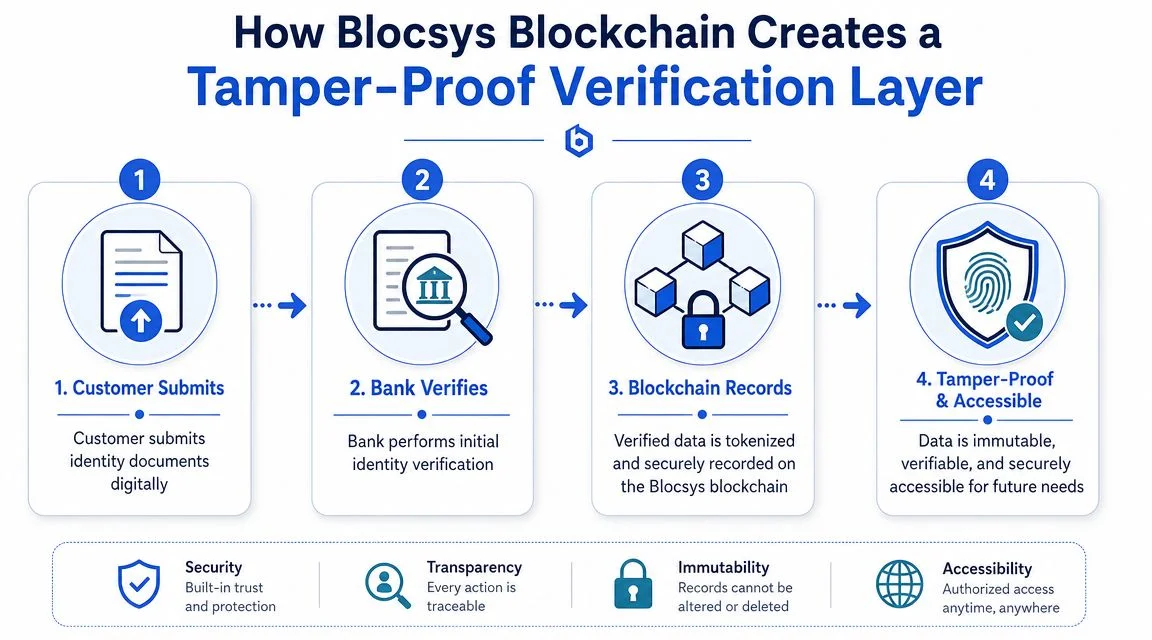

How Blockchain Creates a Tamper-Proof Verification Layer

The most useful way to understand blockchain banking verification is to ignore the hype and focus on evidence handling. A bank doesn’t need a blockchain because documents are digital. It needs one when multiple parties must trust that a verification event happened, that the verified record hasn’t been altered, and that later re-use can be checked without starting over.

What actually goes on-chain

The raw passport, utility bill, company registry extract, or proof-of-address file should not be placed on-chain. The operationally sound pattern is to keep the document off-chain and store only a cryptographic proof and selected metadata on the ledger.

In Indian banking implementations, banks typically use a hash-and-lookup workflow. After KYC documents are collected and validated once, the bank stores an integrity proof on a distributed ledger rather than placing raw personal data on-chain. Another bank can then verify the same customer’s KYC by checking the cryptographic hash, which eliminates redundant onboarding effort, as described in this blockchain KYC workflow paper.

That distinction matters. If the document changes, even slightly, its hash changes. If the document presented later produces a different hash from the verified record, the system can flag the mismatch immediately.

For a plain-language explanation of this integrity model, this overview of digital proof of document integrity is a useful companion.

How the workflow functions in practice

A practical banking flow usually looks like this:

- Document collection. The customer submits KYC material through a digital onboarding journey.

- Primary verification. The issuing bank validates the material using its standard controls, such as OCR, document checks, sanctions screening, and internal review.

- Hash creation. The system generates a cryptographic fingerprint of the verified package.

- Ledger entry. The hash, status, timestamps, and limited verification metadata are written to the shared ledger.

- Reuse event. A second institution receives the customer’s consented verification package and compares the presented material to the ledger proof.

- Decisioning. If the signatures, timestamps, and integrity checks match, the second bank can accept the verified evidence under its own policy rules.

The blockchain record is not the identity. It is the tamper-evident receipt that a defined verification event took place.

The video below gives a useful visual frame for how blockchain-based verification workflows are commonly explained to enterprise audiences.

Comparison Traditional vs. Blockchain Document Verification

| Feature | Traditional Verification | Blockchain-Based Verification |

|---|---|---|

| Evidence trail | Often split across internal systems and reviewer notes | Anchored to a shared, time-stamped ledger entry |

| Reuse across institutions | Usually limited, often requires full resubmission | Designed for controlled re-verification of prior checks |

| Data handling | Raw files copied across repositories | Raw files remain off-chain, proof stored on-chain |

| Tamper detection | Depends on internal controls and versioning discipline | Cryptographic mismatch reveals alteration |

| Auditability | Can be labour-intensive to reconstruct | Easier to verify what was checked and when |

| Customer experience | Repetitive onboarding and duplicate submissions | Lower duplication when verified records are reusable |

| Privacy risk | Central copies can sprawl across systems | Lower when only proofs and minimal metadata are anchored |

Where smart contracts help

Smart contracts are useful when they automate narrow rules, not when they try to replace compliance judgment. Good examples include revocation checks, expiry logic, consent validation, and routing rules for whether a prior verification can be reused.

They are less useful when exceptions are subjective. For example, a slightly inconsistent corporate ownership record may still require a trained analyst. The strongest architecture combines machine-enforced controls with human escalation paths.

A Strategic Blueprint for Implementing Blockchain Verification

Most blockchain verification projects fail because the architecture is treated as a technology choice instead of a trust design problem. The key question is who issues a claim, who holds it, who verifies it later, and what evidence each party can rely on without exposing unnecessary personal data.

Why VC and DID models matter

The strongest technical pattern for reusable banking verification is the verifiable credential and decentralized identifier model. In that flow, an issuer bank signs a credential, the customer presents it to another bank, and the verifier checks validity against the ledger. Reviews of this model also point to the most common failure points: interoperability gaps and weak data-minimisation practices, as outlined in this research on VC and DID-based eKYC models.

The issuer, holder, and verifier structure maps well to real banking roles:

- Issuer bank signs the verified claim after completing onboarding.

- Customer or business user holds the credential and consents to present it.

- Verifier bank checks signature validity, ledger anchoring, and revocation status before accepting it.

This is a better fit for enterprise banking than a simple shared database because it separates possession from proof. The customer controls presentation. The bank controls issuance standards. The verifier controls acceptance policy.

The design decisions banks need to get right

A sound implementation usually depends on five decisions.

- Choose the right ledger model. Most banks prefer permissioned networks for governance, privacy, and participant control.

- Keep personal data off-chain. Only proofs, references, and minimal metadata should be anchored.

- Treat revocation as a first-class feature. A credential that can’t be revoked safely becomes an audit problem later.

- Design for interoperability early. If issuers and verifiers interpret the credential differently, reuse breaks.

- Integrate with existing compliance systems. Core banking, sanctions tools, workflow engines, and case management still do essential work.

A reusable credential is only valuable if every verifier can interpret it the same way and determine whether it is still valid.

Banks also need to align this architecture with privacy obligations. In regulated markets, the challenge isn’t only storing less data. It’s proving purpose limitation, retention logic, and controlled access over time.

Operationally, teams often borrow patterns from wider security automation programmes. This 2026 guide to cyber security automation is useful because it frames a broader lesson that applies here too: automation works best when decision criteria, exception paths, and telemetry are designed upfront.

For institutions mapping enterprise delivery choices, this guide to enterprise blockchain solutions use cases architecture implementation guide is a practical reference.

A practical delivery sequence

A sensible rollout is usually phased, not transformational from day one.

First, define one reusable verification event. Retail KYC refresh, SME onboarding, or inter-entity document verification are common starting points. Then standardise the credential schema and revocation rules before scaling to additional products.

Next, connect the workflow to existing controls rather than bypassing them. OCR, sanctions checks, adverse media screening, and human review remain part of the trust chain.

Finally, test governance before scale. Who can issue? Who can revoke? Who can query? Who can audit? Banks that skip these questions tend to rediscover them under pressure from operations or audit teams.

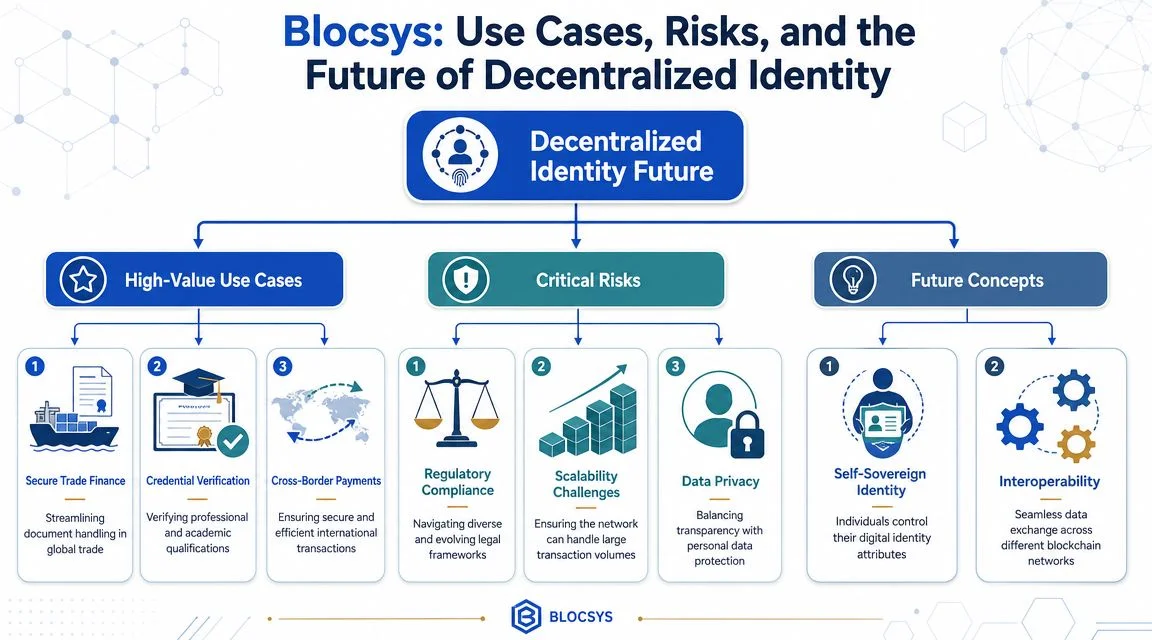

Use Cases, Critical Risks, and the Future of Decentralized Identity

The strongest enterprise use cases are usually the least glamorous. They sit where document handling is repetitive, multi-party, and sensitive to delay. That includes retail onboarding, SME banking, correspondent relationships, and any process where a verified record must move between institutions without becoming a privacy liability.

Where the model creates real value

Three use cases consistently justify the effort.

Cross-bank KYC reuse reduces duplicate document submission when a customer already completed a secure onboarding with another institution.

Corporate and SME verification helps where legal entity records, beneficial ownership evidence, and incorporation documents are repeatedly requested by lenders, payment providers, and treasury teams.

Trade and transaction-adjacent document handling benefits when multiple parties need confidence that a submitted record is authentic, current, and unchanged since approval.

There is also a wider infrastructure angle. India’s digital identity stack showed how electronic KYC can move verification from branch paperwork to machine-readable, time-stamped checks. Aadhaar has over 1.3 billion enrolled residents, making it one of the world’s largest digital identity systems, and its eKYC model demonstrated how digital identity rails can support regulated verification at scale, according to this analysis of Aadhaar-enabled digital public infrastructure.

That doesn’t mean banks should copy the same architecture everywhere. It means they should recognise the operational pattern: verified claims become more useful when they are machine-readable, consented, and auditable.

What blockchain does not fix

These specific issues often cause weak proposals to collapse. Blockchain does not tell a bank whether the original passport was forged, whether the selfie matched a real person, or whether an exception was handled badly.

That gap matters because fraud pressure is real. RBI’s 2024 annual report said banks and financial institutions reported 13,530 fraud cases in FY2023-24, with the reported amount involved rising to ₹36,014 crore, as cited in this discussion of blockchain identity verification and KYC compliance. The hard lesson is simple: if a bad document is verified once and then permanently referenced, the system can preserve a mistake very efficiently.

Banks need a layered model:

- Liveness and biometric checks for remote onboarding

- OCR and forensic document analysis for authenticity screening

- Human review for exceptions and edge cases

- Revocation workflows when prior credentials become unreliable

- Access controls and consent records for every reuse event

Privacy is the second major risk. Shared verification doesn’t automatically mean privacy-preserving verification. Purpose limitation, data minimisation, retention rules, and revocation need to be designed explicitly. This becomes even more important where institutions operate across Europe, the UK, the UAE, Singapore, and other tightly regulated markets.

A good stress test is whether the platform would withstand internal scrutiny from security and risk teams. Resources like this guide to internal pentesting for GRC compliance are useful because they push teams to think about internal trust boundaries, not just external threats.

For teams working on broader identity architecture, blockchain digital identity for securing decentralized data is a relevant internal reference point.

What the next 12 to 24 months will likely reward

The winners in the near term probably won’t be the banks with the most complex ledgers. They’ll be the ones that combine reusable credentials with better onboarding quality, strong consent controls, and measurable auditability.

AI will likely strengthen the front end of the process, especially in anomaly detection, document analysis, and exception routing. Blockchain will remain more useful at the evidence and trust layer than at the decision layer. Decentralized identity models will also gain ground where ecosystem participants agree on credential standards and revocation logic.

The strategic takeaway is straightforward. Banks should invest where blockchain reduces repeated verification and improves trust between institutions, not where it merely adds technical novelty.

Build Your Enterprise-Grade Verification Platform with Blocsys

A production-grade verification platform has to do more than anchor hashes. It needs to fit real operating conditions inside a bank: policy-driven onboarding, exception handling, secure integrations, revocation controls, privacy-aware data flows, and audit evidence that stands up under review.

That is why many institutions need an engineering partner before they need more slideware. The difficult work sits in system design, governance, and integration. Teams have to connect document intake, identity checks, workflow engines, storage layers, credential issuance, verifier APIs, and access controls into one coherent operating model.

One practical option in this space is Blocsys’s tamper-proof document verification platform, which is aligned with the hash-and-proof model discussed above. For banks and fintechs, the value of this kind of platform is not that it replaces compliance operations. It’s that it gives those operations a stronger technical backbone for secure digital proof, controlled reuse, and tamper-evident verification events.

The banks that get this right usually start with a narrow use case, define trust boundaries early, and build the verification layer so it can support additional products later. That is the better route for enterprise banking verification systems, blockchain authentication systems, and decentralized identity verification platforms than trying to overhaul every onboarding journey at once.

Frequently Asked Questions about Blockchain Banking Verification

How does blockchain improve banking document verification

Blockchain improves document verification by creating a tamper-evident record of a verification event. Instead of trusting a copied file or an email trail, a bank can verify a cryptographic proof, timestamp, and signature history. That makes audit trails stronger and document reuse more practical across institutions.

What is blockchain KYC verification

Blockchain KYC verification is a model where a verified customer identity record is represented through proofs, credentials, or hashes that can be checked later without repeating every onboarding step. The most effective versions keep sensitive documents off-chain and store only integrity proofs and related metadata on the ledger.

How do banks use blockchain for customer authentication

Banks generally use blockchain for the verification layer, not as the sole authentication method. A bank verifies the customer once, creates a trusted proof or credential, and then allows another authorised party to validate that proof later. Authentication still depends on broader controls such as login security, consent capture, device trust, and step-up verification where needed.

Does blockchain stop document fraud by itself

No. Blockchain protects record integrity after verification, but it doesn’t prove that the original document was genuine. Banks still need liveness checks, authenticity analysis, sanctions screening, fraud models, and human review for exceptions. Without those controls, a system can preserve false information very effectively.

What are tamper-proof banking verification systems

Tamper-proof banking verification systems are platforms that make it extremely difficult to alter or replace verification evidence without detection. They usually rely on cryptographic hashes, digital signatures, time-stamped records, restricted permissions, and audit logs. In banking, the strongest designs also minimise stored personal data and support revocation.

Why are banks adopting blockchain verification

Banks adopt blockchain verification because repeated KYC and document handling are expensive, slow, and difficult to audit across multiple institutions. A shared verification layer can reduce duplicate onboarding, improve evidence integrity, and create a more reusable trust model for regulated workflows.

How can Blocsys help build blockchain banking verification systems

Blocsys can support the design and build of blockchain-based verification infrastructure by helping teams define the right architecture, select the trust model, design off-chain and on-chain boundaries, implement credential workflows, integrate compliance tools, and create enterprise-ready verification APIs. The goal should be a system that works with banking operations, not one that ignores them.

If your team is evaluating blockchain banking verification, customer document integrity workflows, or decentralized identity infrastructure, Blocsys Technologies can help you assess the architecture, define the operational model, and build a platform that fits real compliance and security requirements. Connect with Blocsys to discuss a practical rollout path for secure banking document authentication and reusable verification at enterprise scale.